April 26, 2026

3 minutes

June 11, 2026

9 minutes

Decentralized finance began as a relatively small experiment within the broader crypto ecosystem. Early protocols focused on replicating simple financial functions: lending, borrowing, trading, and basic payments. At the time, the idea that these systems could evolve into a meaningful layer of global financial infrastructure seemed unlikely to many outside the crypto industry.

Yet over time, DeFi has expanded far beyond its initial phase of experimentation.

What began as isolated applications has evolved into a deeply interconnected ecosystem of financial protocols, liquidity networks, stablecoin systems, and capital markets infrastructure. Today, decentralized finance increasingly resembles an emerging financial system of its own—one with distinct forms of market structure, leverage, liquidity behavior, and systemic risk.

This evolution matters not only for crypto-native participants, but also for institutions, regulators, and traditional financial firms attempting to understand how digital asset markets are changing. DeFi is no longer simply a niche corner of crypto speculation. It is becoming part of a broader transformation in how financial infrastructure may operate in a more digital and programmable economy.

Understanding how DeFi evolved—and why it became increasingly complex—is essential to understanding where the next phase of crypto markets may be headed.

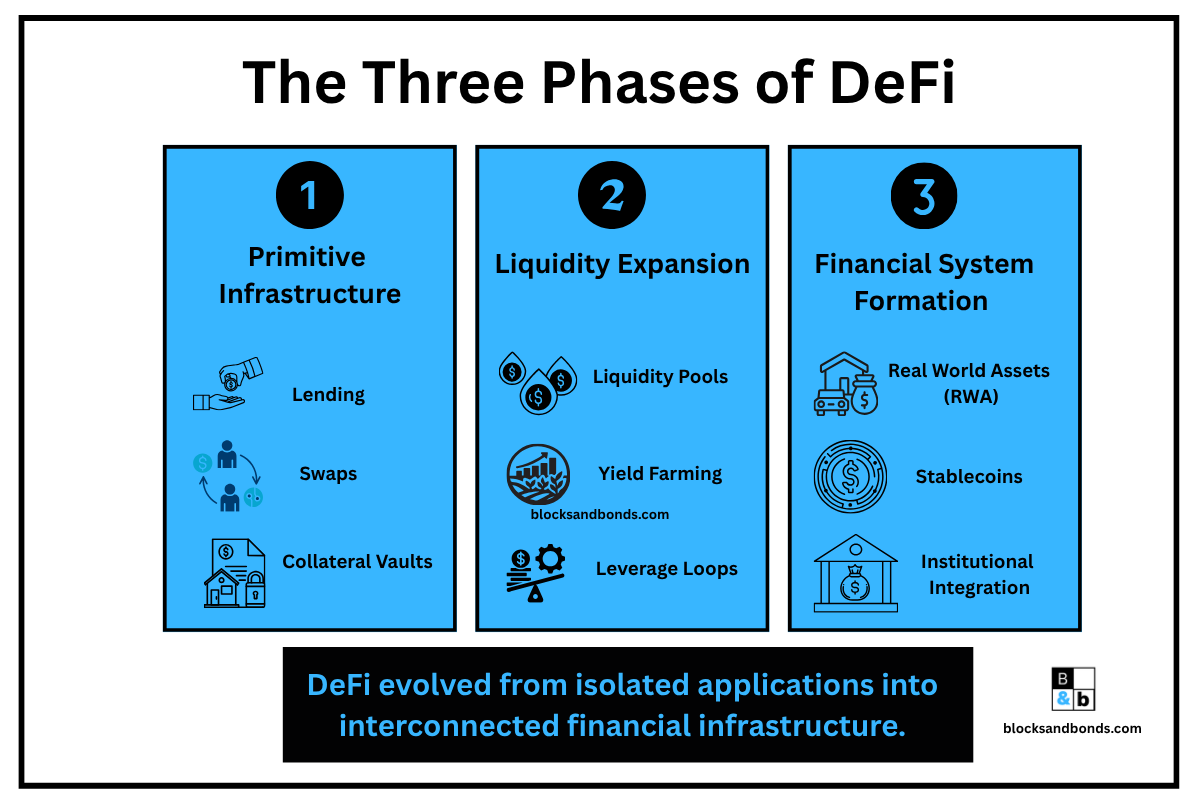

The earliest phase of DeFi focused primarily on recreating basic financial functions using blockchain-based systems.

Protocols such as MakerDAO introduced decentralized stablecoins backed by crypto collateral, while platforms like Compound Labs and Aave enabled users to lend and borrow digital assets without relying on traditional financial intermediaries. At the same time, decentralized exchanges such as Uniswap demonstrated that blockchain-based liquidity pools could facilitate asset trading without centralized order books.

At this stage, DeFi remained relatively simple.

Most protocols operated independently, with limited interaction between systems. Lending platforms handled lending. Exchanges handled trading. Stablecoin systems handled collateral issuance. Users generally interacted with one protocol at a time, and risks were comparatively easier to isolate and understand.

This period was often described as the era of “financial Legos,” where developers built modular applications that could theoretically connect with one another. However, the ecosystem had not yet fully embraced the implications of that composability.

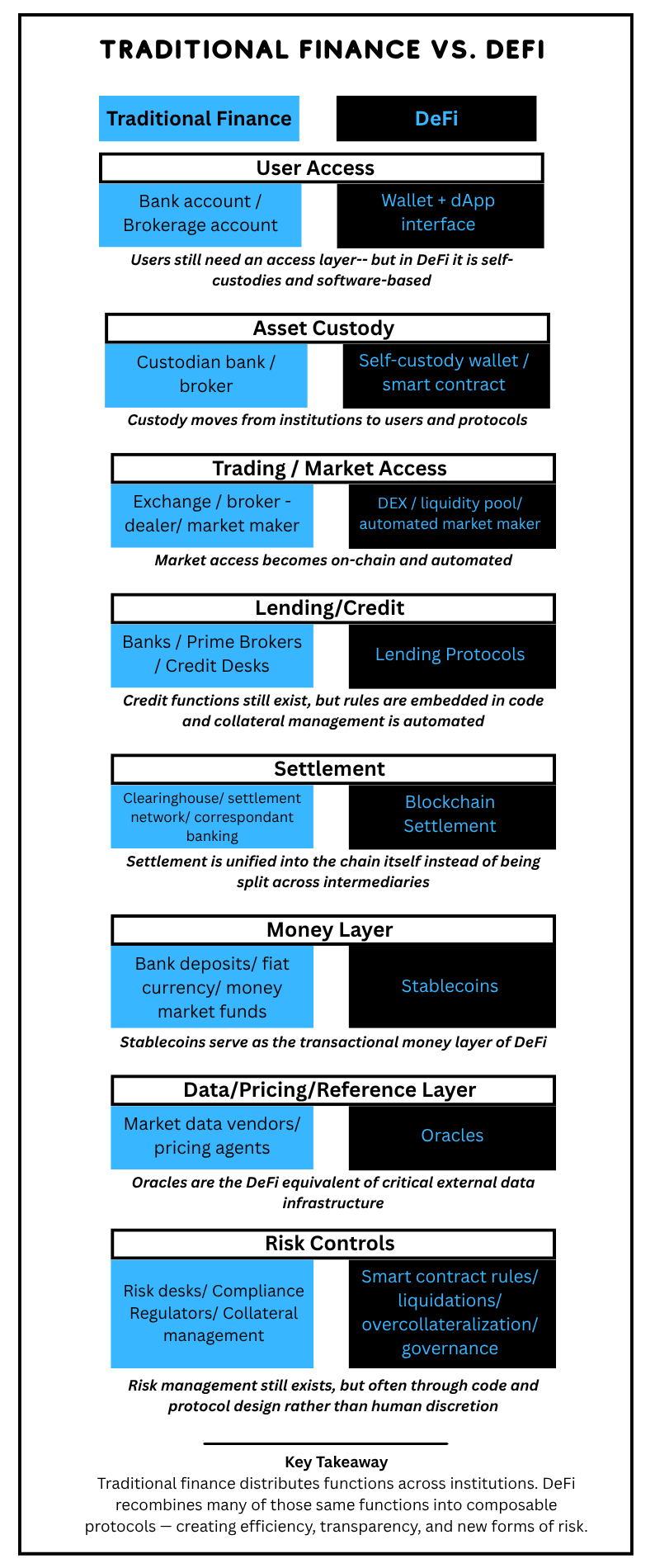

Even in its early form, however, DeFi introduced several structural differences from traditional finance.

First, blockchain-based systems enabled transparent and publicly verifiable transaction histories. Second, smart contracts automated many functions traditionally performed by intermediaries. Third, settlement could occur continuously rather than through restricted banking hours or multi-day clearing processes.

While the scale of the ecosystem remained relatively small, these characteristics attracted a growing community of developers, traders, and investors interested in experimenting with more open and programmable financial systems.

As DeFi matured, protocols began integrating with one another in increasingly sophisticated ways.

This process—commonly referred to as composability—became one of the defining characteristics of decentralized finance. Rather than operating as isolated applications, protocols evolved into interconnected layers of financial infrastructure.

Users could now borrow assets from one protocol, deploy them into liquidity pools on another, stake resulting tokens elsewhere, and use those positions as collateral in additional systems. Capital began flowing continuously through multiple protocols simultaneously.

This represented a major shift in the structure of the ecosystem.

Instead of standalone applications, DeFi increasingly resembled a networked financial system where liquidity, collateral, and market activity became deeply interconnected. A single transaction could trigger activity across multiple protocols, often automatically through smart contracts.

The expansion of liquidity mining and yield farming accelerated this process significantly during the 2020–2021 market cycle. Protocols competed aggressively for user liquidity by offering token incentives, which encouraged increasingly complex strategies designed to maximize returns.

In many cases, users layered leverage on top of leverage.

Assets deposited into one protocol could generate tokens that were then redeployed elsewhere. Stablecoins borrowed against collateral could be used to acquire additional yield-bearing positions. Liquidity itself became highly mobile, moving rapidly between protocols in search of returns.

This increased the overall capital efficiency of the ecosystem, but it also introduced far greater complexity.

DeFi was no longer simply replicating isolated financial services. It was beginning to create a digitally native capital system with its own internal dependencies and feedback loops.

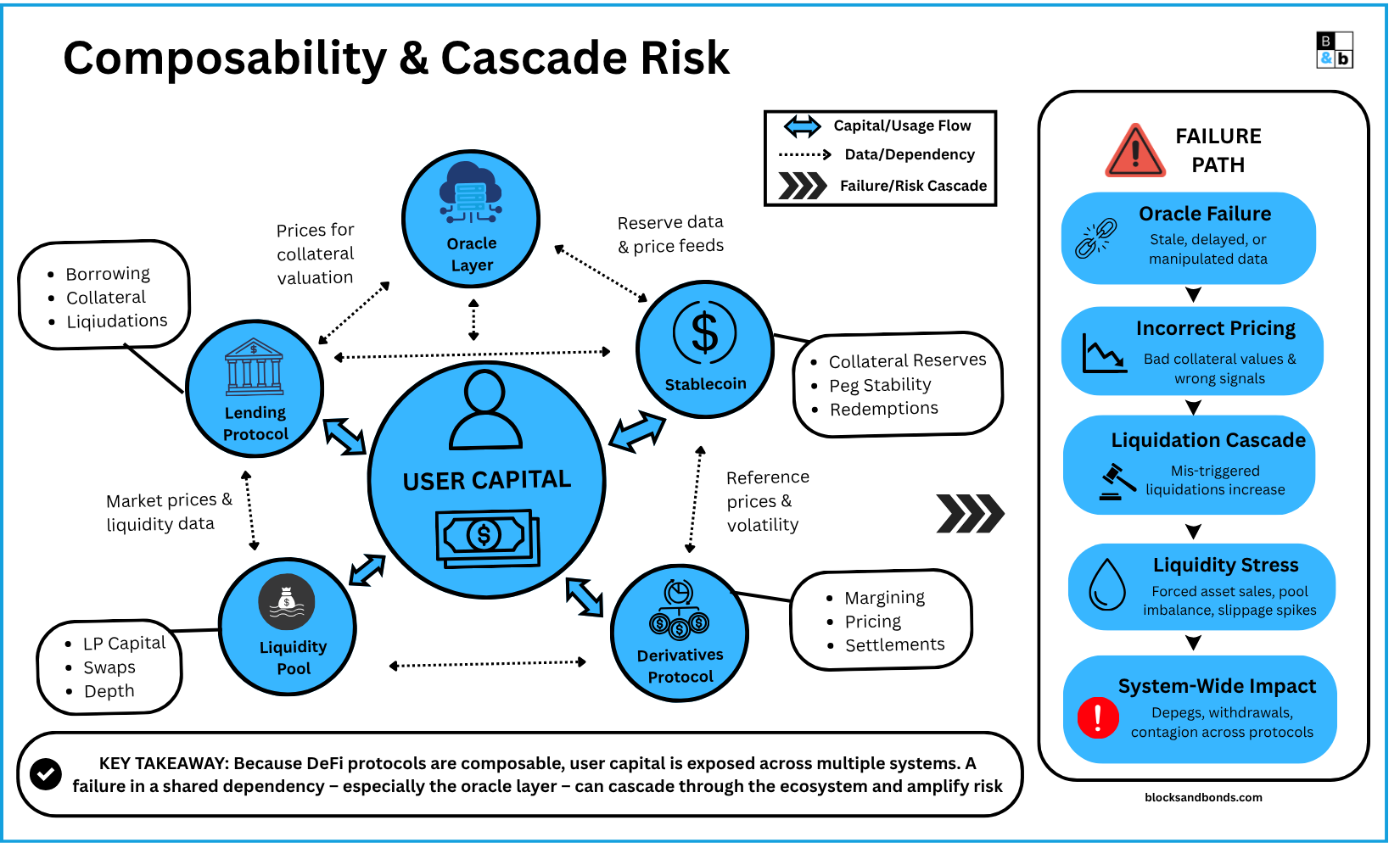

As composability expanded, so did systemic risk.

The interconnected nature of DeFi created conditions where stress in one protocol could spread rapidly throughout the broader ecosystem. Liquidity problems, collateral failures, or pricing disruptions in a single area could trigger cascading effects across multiple platforms.

This dynamic increasingly resembled certain forms of interconnected risk seen in traditional financial markets.

In traditional finance, systemic stress often emerges through chains of leverage, collateral dependencies, and liquidity mismatches. Similar patterns began appearing within DeFi, although expressed through smart contracts and blockchain infrastructure rather than banks and brokerages.

One major source of risk involved liquidation cascades.

Many DeFi lending systems require borrowers to maintain collateral above specified thresholds. When asset prices fall sharply, positions can be automatically liquidated to protect lenders. During periods of volatility, these liquidations can accelerate price declines, which then trigger additional liquidations elsewhere in the system.

The result can become a self-reinforcing cycle:

price declines lead to liquidations, liquidations increase selling pressure, and further selling pressure drives additional declines.

Oracle dependencies created another important layer of risk.

Many protocols rely on external data feeds—known as oracles—to determine asset prices and execute smart contract functions. If pricing data becomes inaccurate, delayed, or manipulated, entire systems may behave unpredictably. Incorrect pricing can trigger unnecessary liquidations, distort collateral values, or create arbitrage opportunities that destabilize markets further.

As protocols became increasingly interconnected, dependency chains also grew more complex.

A stablecoin system might depend on collateral held in lending protocols. Lending protocols might depend on liquidity from decentralized exchanges. Derivatives systems might rely on stablecoin liquidity and external price feeds simultaneously.

This interconnectedness created a structure where failures could propagate across multiple layers of the ecosystem.

In some respects, these dynamics resemble aspects of the traditional shadow banking system, where interconnected leverage and collateral chains can amplify systemic stress during periods of market instability.

The difference is that DeFi exposes many of these relationships publicly and automates their execution through smart contracts. Transparency may improve visibility into risk, but it does not eliminate the underlying fragility created by interconnected leverage and liquidity dependencies.

Despite these risks, the pursuit of greater capital efficiency has remained one of the primary drivers of DeFi innovation.

Traditional financial systems often contain significant operational friction and idle capital. Settlement delays, intermediary layers, geographic fragmentation, and restricted access can reduce the efficiency of how capital moves through markets.

DeFi protocols attempted to address these inefficiencies by making financial infrastructure more programmable and interoperable.

Collateral could be reused more dynamically. Liquidity could move continuously between applications. Settlement could occur automatically through smart contracts. Market access became increasingly global and continuous.

This flexibility enabled rapid experimentation with new financial structures.

Protocols introduced synthetic assets, decentralized derivatives markets, algorithmic stablecoins, structured yield products, and automated liquidity mechanisms. In many cases, these innovations developed far more quickly than comparable products in traditional financial systems because blockchain infrastructure allowed developers to deploy and iterate rapidly.

At the same time, however, increasing sophistication also made the ecosystem more difficult to analyze.

Understanding risk increasingly required understanding not just individual protocols, but the relationships between them. Market participants needed to evaluate liquidity dependencies, collateral structures, governance incentives, and systemic exposure across multiple layers of infrastructure.

As DeFi evolved, it became less like a collection of applications and more like an emerging digital financial architecture.

For years, institutional firms largely viewed DeFi as speculative, unstable, or operationally immature.

That perception has gradually begun to change.

While many institutions remain cautious, several underlying themes within DeFi have attracted growing attention from traditional financial firms and infrastructure providers.

One major factor is programmability.

Smart contracts allow financial agreements, collateral rules, and settlement processes to execute automatically according to predefined logic. This introduces the possibility of reducing operational friction, improving settlement efficiency, and creating more transparent financial infrastructure.

Stablecoins have also played an important role in shifting institutional perceptions.

As stablecoin systems matured, they increasingly demonstrated how blockchain-based payment and settlement infrastructure could operate continuously across global markets. This has implications not only for crypto trading, but also for broader payment systems, treasury management, and capital markets infrastructure.

At the same time, tokenized real-world assets (RWAs) have created new connections between DeFi infrastructure and traditional finance.

Tokenized Treasury products, on-chain money market structures, and blockchain-based settlement systems suggest that elements of decentralized infrastructure may eventually integrate with institutional capital markets rather than remain entirely separate from them.

Importantly, institutional interest in DeFi does not necessarily mean institutions are embracing fully permissionless systems.

Instead, many firms are exploring more controlled or compliant forms of blockchain-based financial infrastructure:

- permissioned liquidity systems,

- regulated tokenized assets,

- institutional stablecoins,

- and blockchain-based settlement networks.

This reflects a broader shift in perception: DeFi is increasingly viewed not simply as speculative crypto infrastructure, but as a potential model for more programmable financial systems.

As the ecosystem matures, DeFi is likely to evolve in several important ways.

First, user experience and infrastructure abstraction will likely improve significantly. Much of today’s DeFi ecosystem remains operationally complex for average users. Over time, interfaces may simplify while blockchain infrastructure becomes increasingly invisible beneath financial applications.

Second, regulation will likely play a larger role.

As stablecoins, tokenized assets, and blockchain settlement systems become more integrated into global financial markets, regulators will place greater emphasis on compliance, custody standards, market structure, and systemic risk oversight.

Third, institutional participation may deepen gradually.

Rather than replacing traditional finance outright, DeFi infrastructure may increasingly merge with existing capital systems. Elements of decentralized architecture could become embedded within broader financial infrastructure while operating alongside regulated intermediaries.

Finally, market structure itself may continue evolving toward greater integration between crypto markets and traditional financial systems.

Liquidity, macroeconomic conditions, interest rate expectations, and institutional positioning are already influencing digital asset markets more directly than in earlier phases of crypto development. As institutional participation grows, these relationships may strengthen further.

The result may not be a fully decentralized financial world, nor a simple continuation of traditional finance.

Instead, the next phase of DeFi may involve the gradual emergence of hybrid financial infrastructure—combining blockchain-based programmability with institutional capital, regulated systems, and global digital settlement networks.

DeFi has moved far beyond its original phase of experimentation.

What began as a collection of isolated protocols has evolved into a complex ecosystem of interconnected financial infrastructure, liquidity systems, and programmable capital markets. Along the way, decentralized finance introduced new forms of efficiency, transparency, and financial coordination—but also new forms of systemic complexity and risk.

The evolution of DeFi reflects a broader shift occurring across digital finance:

financial infrastructure itself is becoming increasingly programmable, interconnected, and globally accessible.

Whether decentralized finance ultimately transforms the financial system entirely or becomes integrated into existing institutional structures, its development is already reshaping how markets think about liquidity, settlement, collateral, and capital movement in a digital economy.