March 1, 2026

2 min

March 18, 2026

Tokenization is often described as the process of placing real-world assets on blockchain networks. This framing emphasizes the role of technology—smart contracts, distributed ledgers, and digital tokens.

In practice, tokenization depends less on code than on legal structure. A token does not create ownership on its own. It represents a claim that must be defined, recognized, and enforceable within existing legal systems.

For this reason, the development of tokenized assets is fundamentally shaped by what can be described as legal architecture: the combination of entities, contracts, and regulatory frameworks that define how ownership is created and maintained.

Understanding this architecture is essential to evaluating whether a tokenized asset is credible financial infrastructure or simply a digital representation without enforceable rights.

A tokenized asset is not the asset itself. It is a representation of a claim.

That claim may refer to:

• ownership of an underlying asset

• a beneficial interest in a legal entity

• a contractual right to cash flows

• a redemption mechanism tied to an asset pool

The nature of the claim determines what the token actually conveys.

In many tokenized structures, investors do not directly own the underlying asset. Instead, they hold tokens linked to a legal entity—such as a fund or special purpose vehicle—that owns the asset.

This distinction is critical. Without a clear legal relationship between the token and the underlying asset, the token may not provide meaningful rights.

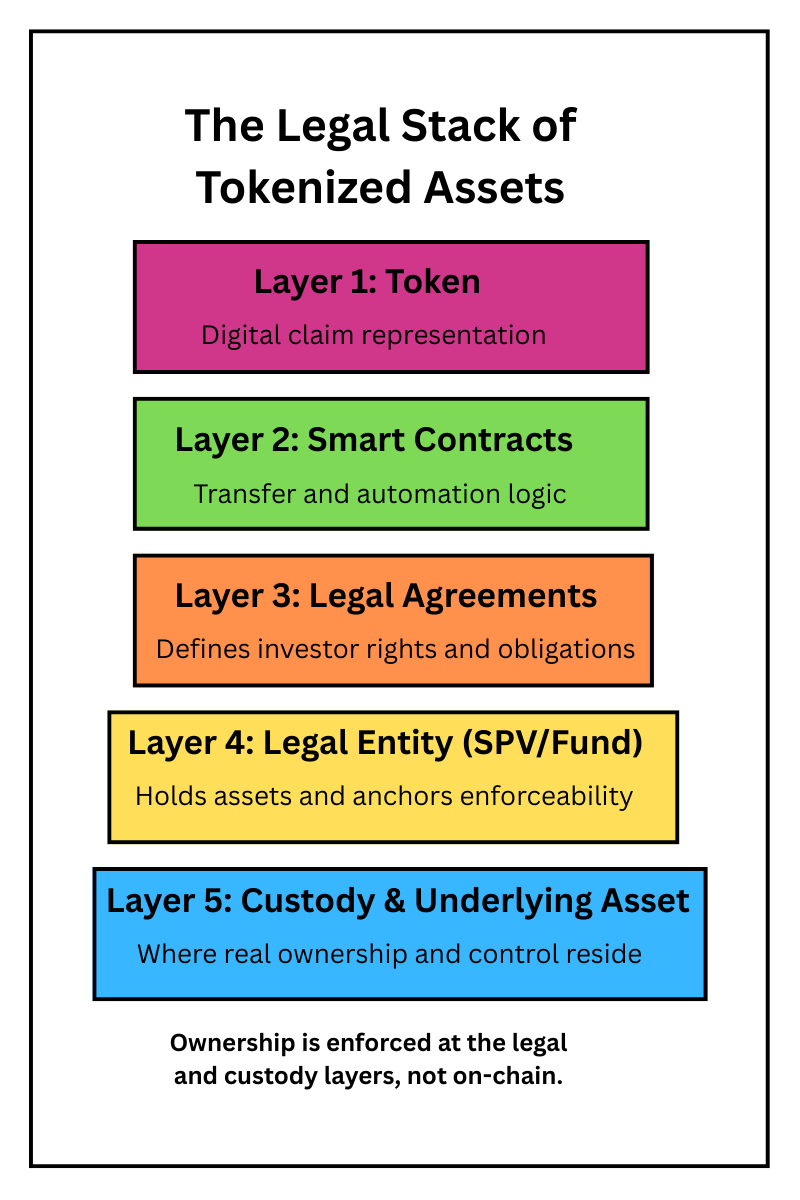

Tokenized assets rely on several interconnected layers of legal structure.

Most tokenized assets are issued through legal entities such as funds, trusts, or special purpose vehicles (SPVs).

These entities:

• hold the underlying assets

• define investor rights

• provide a point of legal accountability

The entity is often the true anchor of the structure, not the token itself.

Investor rights are defined through legal agreements.

These may include:

• redemption rights

• income distribution terms

• governance provisions

• bankruptcy treatment

Smart contracts can automate certain processes, but they do not replace legal agreements.

Custodians play a central role in holding and safeguarding the underlying assets.

They also provide:

• operational control

• regulatory compliance

• interaction with traditional financial systems

Custody is where legal ownership and operational control converge.

Tokenized assets must operate within regulatory regimes that govern securities, funds, and financial markets.

These frameworks determine:

• who can invest

• how products are structured

• disclosure requirements

• compliance obligations

Regulation is not external to tokenization. It is part of the architecture.

Blockchain systems can record transactions and automate transfers. They cannot, on their own, enforce ownership in courts or resolve disputes.

If a token holder’s claim is challenged, the outcome depends on:

• the legal entity structure

• contractual documentation

• jurisdictional law

This means that the credibility of a tokenized asset is determined less by the sophistication of its smart contracts and more by the strength of its legal framework.

In this sense, tokenization does not eliminate traditional financial infrastructure. It reconfigures how it is represented and accessed.

One of the key challenges in tokenized assets is jurisdictional variation.

Different regions may treat tokenized assets differently in terms of:

• securities classification

• custody requirements

• investor protections

• tax treatment

A structure that is viable in one jurisdiction may not be transferable to another.

This fragmentation limits scalability and introduces complexity for global investors.

Tokenization is often associated with the idea of direct ownership—where a token represents a direct claim on an asset without intermediaries.

In practice, most tokenized assets still rely on intermediaries such as:

• custodians

• administrators

• legal entities

These intermediaries are not eliminated. They are reorganized.

Understanding this helps explain why tokenization has progressed fastest in institutional contexts where these structures already exist.

The importance of legal architecture explains several patterns in tokenized asset adoption.

First, tokenization has advanced most rapidly in assets with clear legal frameworks, such as Treasuries and money market funds.

Second, more complex assets—such as private credit or real estate—face slower adoption due to legal complexity and uncertainty.

Third, institutional participation depends heavily on whether tokenized structures meet existing legal and compliance standards.

These dynamics suggest that tokenization will expand unevenly, shaped by legal feasibility rather than technological possibility.

Tokenized assets are often described in terms of technology, but their success depends on legal design.

A token is only as meaningful as the rights it represents and the structures that enforce those rights. Without a robust legal architecture, tokenization risks becoming a superficial layer that does not deliver true ownership or protection.

As tokenized markets develop, the key question will not be how sophisticated the technology becomes, but how effectively legal frameworks can support and scale these new forms of financial infrastructure.