March 1, 2026

2 min

March 18, 2026

Tokenization is often framed as a broad transformation of financial markets. In theory, any asset—from real estate to private equity—can be represented on blockchain infrastructure. In practice, adoption has been far more selective.

One of the most significant early areas of traction has been tokenized money market funds, particularly those backed by U.S. Treasuries. These products combine traditional short-term government securities with blockchain-based distribution and settlement mechanisms.

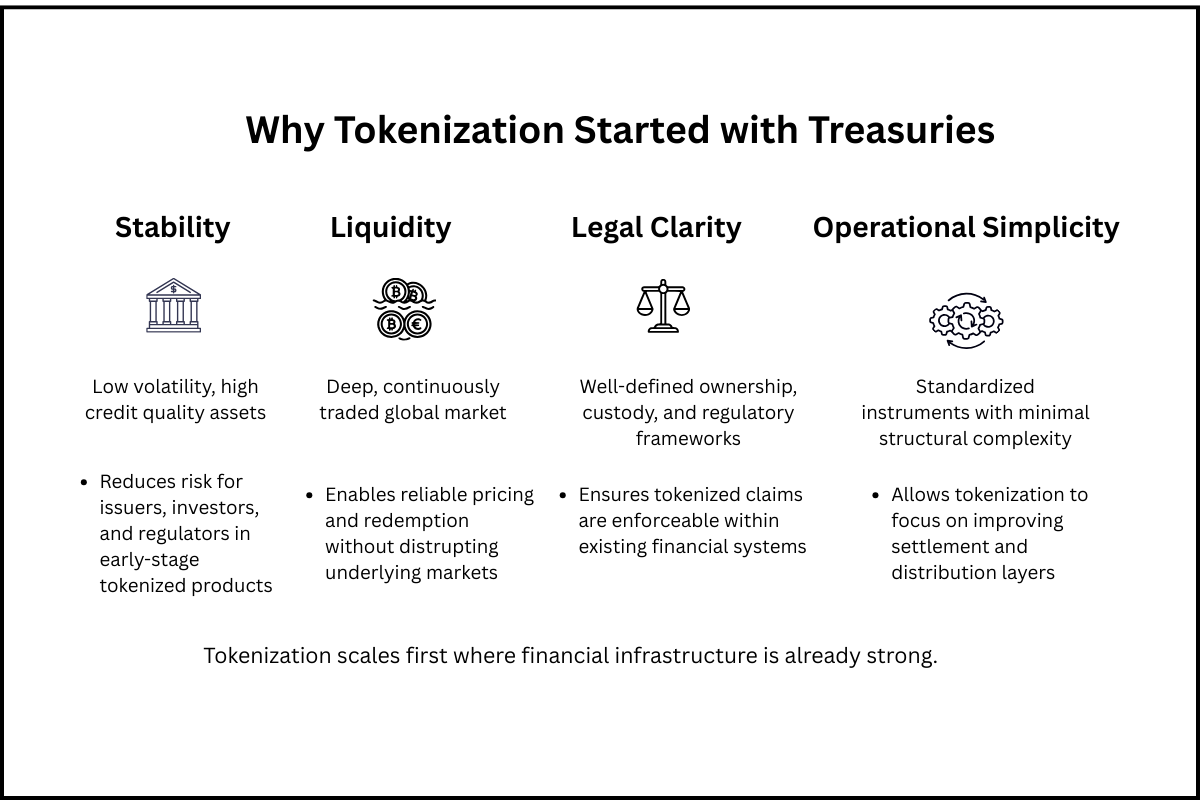

The concentration of activity in this segment is not accidental. It reflects the underlying requirements of financial infrastructure: stability, liquidity, and legal clarity.

Understanding why Treasuries came first provides a clearer view of how tokenized assets are likely to develop across broader markets.

Tokenized money market funds are investment vehicles that hold short-term, highly liquid assets—typically U.S. Treasuries or similar government securities—and issue blockchain-based tokens representing investor claims.

Structurally, these products resemble traditional money market funds. They provide:

• exposure to low-risk, short-duration assets

• daily liquidity or near-daily redemption

• yield derived from underlying government securities

The difference lies in how ownership is represented and transferred. Instead of relying solely on traditional fund administration systems, these products use blockchain networks to enable:

• digital ownership records

• programmable transfers

• integration with on-chain financial systems

In most cases, the blockchain layer does not replace the legal and custodial structure of the fund. It sits alongside it, creating a hybrid system.

The early dominance of Treasury-backed products reflects several structural advantages.

Treasuries are widely considered among the lowest-risk financial assets. For tokenized products seeking institutional adoption, this stability is essential.

Higher-risk or more complex assets introduce valuation uncertainty and regulatory scrutiny, both of which slow adoption.

The U.S. Treasury market is one of the most liquid markets in the world. This liquidity supports reliable pricing, efficient redemption mechanisms, and the ability to scale.

Tokenized products require underlying assets that can be bought and sold without disrupting market conditions. Treasuries meet this requirement.

Perhaps most importantly, Treasuries operate within well-established legal and regulatory frameworks.

Ownership rights, settlement processes, and custody arrangements are clearly defined. This reduces uncertainty for both issuers and investors.

Tokenization does not eliminate the need for legal enforceability. In many cases, it makes it more important.

Compared to other asset classes, Treasuries are relatively straightforward to administer.

They do not require complex valuation models, extensive due diligence, or bespoke legal structures. This simplicity allows tokenized products to focus on improving distribution and settlement, rather than solving underlying asset complexity.

The resurgence of interest in tokenized money market funds has also been influenced by macroeconomic conditions.

Higher interest rates have made short-term government securities more attractive. As yields increased, the opportunity cost of holding idle capital grew.

Tokenized Treasury products offer a way to combine:

• yield from traditional assets

• flexibility of blockchain-based settlement

This combination has made them particularly appealing in digital asset markets, where capital can move quickly between on-chain and off-chain environments.

Tokenized money market funds are currently used in several ways.

In digital asset markets, these products provide a yield-bearing alternative to holding stablecoins.

Participants can move capital into tokenized Treasuries to earn yield while maintaining the ability to re-enter markets relatively quickly.

Tokenized Treasuries can also function as collateral in certain financial applications.

Their stability and liquidity make them suitable for use in lending, trading, and other financial transactions where reliable collateral is required.

Some institutional investors are beginning to explore tokenized funds as a way to access short-term assets with enhanced operational flexibility.

However, this use case remains early and is heavily dependent on regulatory clarity and infrastructure development.

The success of tokenized Treasury products highlights a broader pattern in financial innovation.

Tokenization is not expanding evenly across all asset classes. It is progressing first in areas where:

• assets are standardized

• markets are liquid

• legal frameworks are well established

• operational complexity is low

These conditions reduce risk and allow tokenization to focus on improving infrastructure rather than redefining the underlying asset.

Despite their early success, tokenized money market funds face several limitations.

Liquidity in secondary markets remains limited, and many products rely on issuer redemption rather than continuous trading.

Custody and operational integration continue to present challenges, particularly for institutional investors.

Regulatory treatment also varies across jurisdictions, which can limit scalability.

These constraints suggest that while tokenized Treasuries are an important starting point, they are not a complete solution.

Tokenized money market funds represent one of the first credible applications of tokenization within traditional financial markets.

Their focus on Treasuries reflects the fundamental requirements of financial infrastructure: stability, liquidity, and legal clarity.

Rather than transforming financial markets overnight, these products demonstrate how tokenization is likely to evolve—incrementally, and within existing systems.

If Treasuries are the starting point, the next phase of tokenization will depend on whether similar conditions can be established for more complex asset classes.