March 1, 2026

3 minutes

May 13, 2026

5 minutes

For years, stablecoins were often framed as a challenge to the traditional banking system.

The assumption was straightforward: if blockchain networks enabled users to move digital dollars without banks, then stablecoins would eventually bypass financial institutions altogether.

Instead, a more complex reality is emerging.

Rather than disappearing from the system, banks are increasingly positioning themselves as critical participants in the stablecoin economy:

The result is not necessarily a replacement of banking infrastructure, but the gradual integration of blockchain-based payment rails into existing financial systems.

Stablecoins may change how money moves, but banks still play a central role in how trust, regulation, liquidity, and financial access are managed.

Despite their digital-native appearance, most major stablecoins remain deeply connected to the traditional financial system.

A dollar-backed stablecoin typically relies on:

Even the issuance and redemption process itself often requires traditional banking relationships.

When users convert dollars into stablecoins or redeem stablecoins back into fiat currency, banks frequently sit somewhere within that flow.

This is one reason why stablecoin adoption increasingly looks less like “debanking” and more like a hybrid financial architecture.

Blockchain networks may provide the settlement rails, but traditional institutions still anchor much of the underlying liquidity and trust structure.

Banks historically move cautiously when new financial infrastructure emerges.

But stablecoins increasingly align with several areas banks already care deeply about:

Large financial institutions increasingly recognize that stablecoins are not simply speculative crypto products.

They represent:

In many ways, stablecoins resemble an evolution of payments technology more than an entirely separate financial ecosystem.

This is particularly important as global payment competition intensifies and fintech firms continue pressuring traditional banking models.

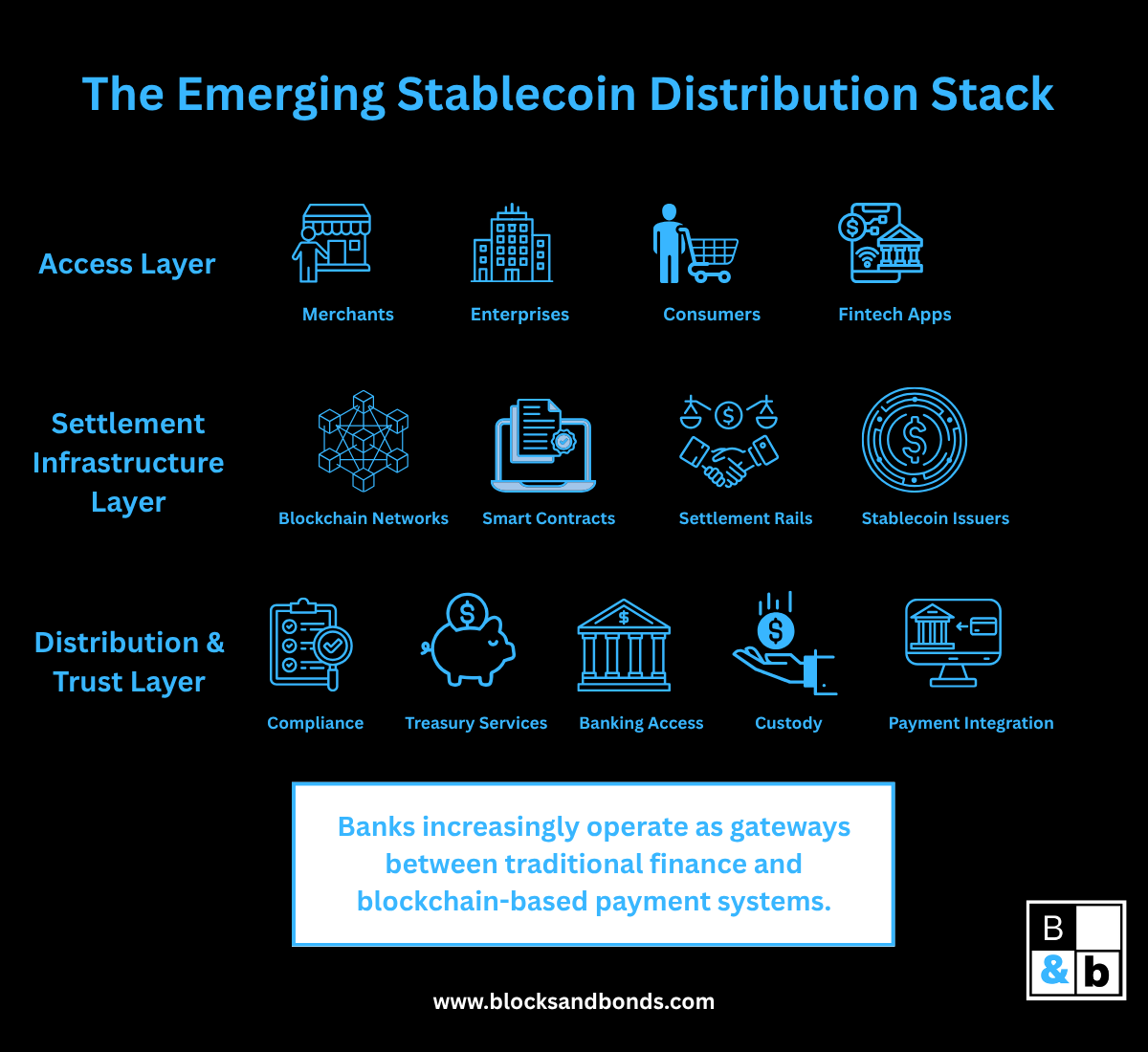

One of the most important developments in the stablecoin market is the growing distinction between issuance and distribution.

Many discussions focus on who creates stablecoins.

But over time, distribution may become equally important:

Banks already possess several advantages in distribution:

This may position banks less as competitors to stablecoins and more as gateways into stablecoin-based financial systems.

In practice, many users may eventually access stablecoin rails through traditional financial interfaces:

The blockchain layer may remain largely invisible to end users.

One reason banks are approaching stablecoins carefully is that deposits remain central to modern banking models.

Traditional banks rely heavily on customer deposits to support lending, liquidity management, and broader balance sheet operations.

Stablecoins introduce new competitive dynamics:

This creates both risks and opportunities for banks.

Some institutions may eventually issue tokenized deposits or bank-backed digital payment instruments that operate alongside public stablecoins.

Others may focus on becoming trusted distribution and custody partners rather than issuers themselves.

The broader outcome may not be a single “winner,” but a layered ecosystem involving:

One of the clearest trends in stablecoin adoption is the growing importance of compliance infrastructure.

Large enterprises and financial institutions generally require:

Banks already specialize in many of these functions.

As a result, institutions with strong compliance frameworks may become increasingly important participants in stablecoin distribution networks.

This helps explain why some stablecoin strategies increasingly emphasize:

The future of stablecoin adoption may depend less on avoiding regulation and more on integrating effectively with regulated financial systems.

Historically, banks controlled much of the infrastructure surrounding payments, deposits, and settlement.

Stablecoins expand that infrastructure into programmable digital networks.

But rather than eliminating banks, this transition may redistribute responsibilities across a broader financial stack.

Blockchain networks may increasingly handle:

Banks may increasingly focus on:

The financial system may gradually evolve toward a hybrid model where traditional institutions and blockchain infrastructure operate together rather than independently.

The relationship between banks and stablecoins is becoming increasingly collaborative rather than purely competitive.

Stablecoins may modernize how value moves across financial systems, but banks still provide many of the trust, compliance, liquidity, and distribution functions large-scale finance depends on.

The emerging question is no longer whether banks will interact with stablecoins.

It is how deeply stablecoin infrastructure will become integrated into banking itself.

Over time, many consumers and businesses may access blockchain-based payment systems through familiar financial institutions without ever directly interacting with the underlying technology.

And in that environment, the institutions that succeed may not simply be the ones issuing digital assets.

They may be the ones controlling access to the infrastructure layer beneath them.