March 1, 2026

3 minutes

Scott Kasten

March 16, 2026

6 minutes

Stablecoins are increasingly discussed as a new layer of financial infrastructure. Much of the attention has focused on their role in cryptocurrency markets or their potential to disrupt traditional payments. In practice, the early stages of adoption are more incremental.

Enterprises are beginning to experiment with stablecoins in specific operational contexts—particularly where existing financial infrastructure introduces delays, costs, or complexity. At the same time, banks are not passive observers. They are evaluating how stablecoins fit within existing financial systems and how to position themselves as this infrastructure evolves.

Understanding the trajectory of stablecoins therefore requires looking at two dynamics simultaneously:

These two forces will shape how stablecoins integrate into the broader financial system.

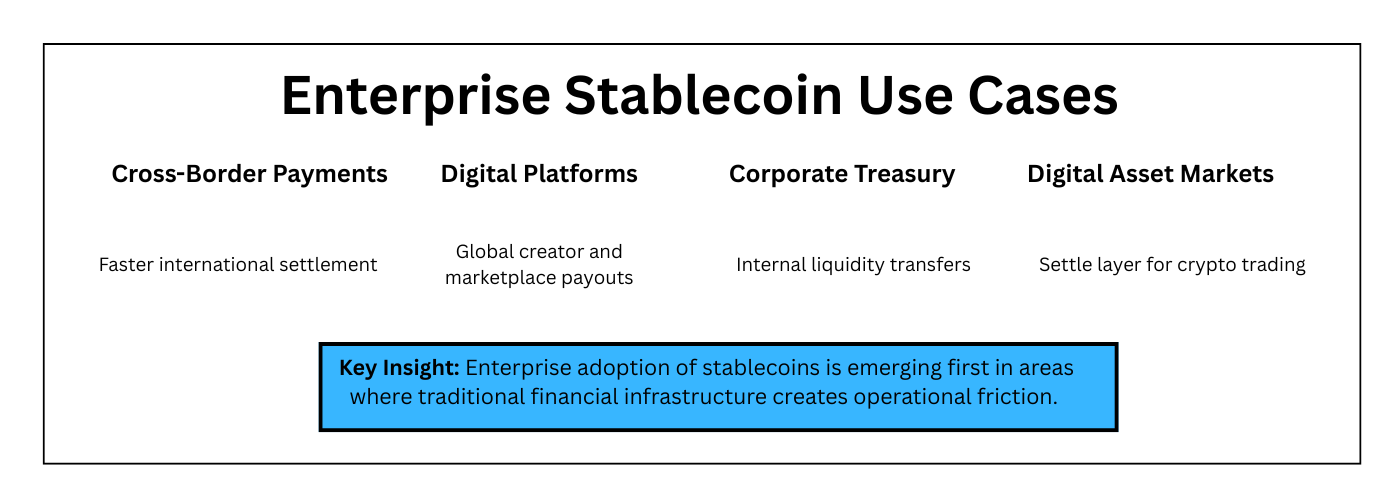

Enterprise use of stablecoins remains selective, but several patterns are becoming visible. Adoption tends to occur where stablecoins offer clear improvements over existing systems rather than where they require wholesale replacement of financial infrastructure.

One of the most frequently discussed enterprise use cases for stablecoins is cross-border payments. Traditional international transfers often pass through multiple correspondent banking relationships and can take several days to settle.

Stablecoin transfers offer a different model. Funds can move across blockchain networks in minutes, and the settlement process can occur outside the constraints of traditional banking hours.

For companies operating globally, this can reduce delays associated with moving funds between subsidiaries, paying suppliers in different jurisdictions, or managing international liquidity.

Several fintech companies and payment providers are already experimenting with stablecoin-based settlement for cross-border flows, particularly in regions where traditional banking infrastructure is slower or more expensive.

Stablecoins are also increasingly relevant for digital platforms that operate across multiple jurisdictions.

Online marketplaces, gaming platforms, and digital service providers often need to manage payments between users located in different countries. Stablecoins provide a standardized digital asset that can move easily across borders without requiring currency conversion through multiple intermediaries.

For platform operators, this can simplify the process of:

• paying creators or contributors

• distributing platform earnings

• managing global digital transactions

While many platforms still rely primarily on traditional payment systems, stablecoins are beginning to appear as an additional settlement option in certain digital ecosystems.

Another emerging use case involves corporate treasury operations.

Companies frequently move funds between internal accounts, subsidiaries, and financial partners. In traditional systems these transfers may involve delays associated with banking hours, settlement processes, and reconciliation procedures.

Stablecoins introduce the possibility of near-real-time movement of digital dollars between accounts operating on blockchain infrastructure.

For treasury teams, potential benefits include:

• faster internal fund transfers

• improved liquidity visibility

• reduced settlement delays

However, adoption in this area remains cautious. Treasury departments must consider regulatory compliance, custody solutions, and integration with accounting and reporting systems.

Enterprises participating in digital asset markets represent another early area of stablecoin usage.

Trading firms, payment companies, and fintech platforms often use stablecoins as settlement assets within digital markets because they provide price stability while remaining compatible with blockchain infrastructure.

In these environments, stablecoins can function as the settlement layer connecting trading systems, liquidity pools, and financial platforms.

While this use case remains closely tied to crypto-native markets, it demonstrates how stablecoins can operate as infrastructure rather than speculative assets.

As stablecoins expand into enterprise use cases, banks face a strategic question: how should they respond to a new form of settlement infrastructure that operates partially outside traditional systems?

Banks are unlikely to adopt a single uniform approach. Instead, three distinct strategic paths are emerging.

In this model, banks integrate stablecoins into their existing services.

This may include:

• supporting stablecoin-based payments

• providing custody for digital assets

• offering fiat on/off-ramps

• enabling enterprise clients to use stablecoin settlement

Under this approach, banks remain central to the financial system by extending their services into new infrastructure layers.

This path aligns with the historical role of banks as intermediaries that adapt to new technologies while maintaining control over key financial relationships.

Some banks may move beyond integration to issuing their own stablecoins or participating directly in stablecoin networks.

This approach allows banks to:

• control settlement mechanisms

• maintain direct relationships with enterprise clients

• capture value within the payment infrastructure itself

Examples include bank-issued digital dollars or tokenized deposit systems.

This path represents a more proactive strategy, positioning banks not just as participants but as infrastructure providers.

A third group of banks may take a more cautious approach.

Rather than actively integrating or issuing stablecoins, they may:

• limit exposure to stablecoin-related activities

• focus on regulatory clarity

• reinforce existing payment systems

• engage selectively with stablecoin infrastructure

This approach reflects concerns around regulatory risk, operational complexity, and potential disintermediation.

However, over time, even defensive positioning may require some level of engagement as enterprise demand evolves.

These three paths are not mutually exclusive. In practice, the financial system is likely to evolve into a hybrid modelwhere:

• stablecoins provide new settlement rails

• banks provide compliance, custody, and financial services

• enterprises use both systems depending on the use case

Rather than replacing traditional finance, stablecoins are more likely to become embedded within it.

Despite growing interest, several constraints continue to shape the pace of adoption.

Regulatory clarity remains uneven across jurisdictions, making large-scale enterprise deployment difficult.

Custody and operational integration also present challenges. Enterprises must ensure that stablecoin systems align with existing financial processes and risk management frameworks.

Finally, trust remains a central factor. Stablecoins must demonstrate reliability and stability under real market conditions to gain widespread institutional acceptance.

For financial institutions, enterprise experimentation with stablecoins is an early indicator of how blockchain-based settlement systems may integrate with traditional finance.

Banks, payment providers, and infrastructure companies are increasingly exploring how stablecoins could support areas such as cross-border settlement, digital commerce, and liquidity management.

Rather than replacing existing payment infrastructure overnight, stablecoins are more likely to appear as an additional settlement layer within hybrid financial systems.

The pace of adoption will depend on regulatory frameworks, infrastructure development, and the ability of stablecoin systems to integrate with established financial networks.

Enterprise adoption of stablecoins is not occurring as a broad shift away from traditional finance. Instead, it is emerging through targeted use cases where blockchain-based settlement offers clear operational advantages.

At the same time, banks are actively evaluating how to position themselves within this evolving landscape. Whether through integration, issuance, or cautious engagement, their response will play a central role in determining how stablecoins develop as financial infrastructure.

The future of stablecoins is therefore unlikely to be defined by disruption alone. It will be shaped by the interaction between new settlement technologies and the institutions that have long governed the movement of money.