March 1, 2026

3 min

April 25, 2026

Stablecoins have quietly crossed a critical threshold. What began as a niche tool for crypto trading has evolved into a functional layer of global financial infrastructure. Today, stablecoins are increasingly used for settlement, payments, treasury management, and cross-border value transfer—often operating faster, cheaper, and with greater programmability than legacy payment systems.

This shift marks a transition in how stablecoins should be understood. They are no longer best described as “crypto assets.” Instead, they are emerging as digital settlement instruments, combining elements of money market funds, payment rails, and programmable software. The result is a new financial stack—one that sits alongside, and increasingly integrates with, banks, payment processors, and enterprise systems.

Three structural forces are driving this transformation.

First, payments—not speculation—have become the dominant stablecoin use case. While trading volumes remain significant, growth is increasingly concentrated in real-world applications: cross-border payments, B2B settlement, merchant payouts, global payroll, and internal treasury operations. In these contexts, stablecoins function less like volatile assets and more like digital cash with global reach.

Second, blockchains are being repurposed as settlement layers. Public blockchains—particularly those optimized for speed, cost, and finality—are increasingly used as neutral, always-on settlement networks. In this model, blockchains resemble interbank clearing systems more than consumer-facing applications. The value accrues not from speculation, but from reliable execution, atomic settlement, and reduced reconciliation.

Third, regulation is shifting from uncertainty to structure. Across major jurisdictions, policymakers are no longer debating whether stablecoins should exist, but how they should be supervised. Compliance requirements—reserve transparency, licensing, transaction monitoring, and consumer protections—are becoming defining features of “payment-grade” stablecoins. Far from stifling adoption, regulatory clarity is increasingly acting as a moat, separating scalable infrastructure from experimental finance.

Together, these forces are reshaping the stablecoin ecosystem into a layered stack:

This report examines each layer of that stack in detail, with a focus on four core areas: issuers, settlement infrastructure, compliance frameworks, and bank integration. It analyzes how value and control are distributed across the stack, where incumbents retain advantages, and where new entrants are creating leverage.

A central conclusion emerges: stablecoins are not replacing banks or payment networks—they are rewiring how money moves between them. Banks are experimenting with issuance, custody, and settlement. Payment companies are integrating stablecoins as back-end rails. Enterprises are adopting stablecoins not for ideological reasons, but because they solve concrete operational problems.

.png)

Over the next 12–36 months, the most important developments will not be driven by consumer speculation, but by institutional adoption: payment-grade issuance, bank-native stablecoins, deeper integration with treasury systems, and increasing interoperability with tokenized real-world assets. The stablecoin stack is solidifying into infrastructure—quietly, incrementally, and with lasting impact.

For financial institutions, enterprises, and policymakers, the question is no longer if stablecoins matter, but where they fit within the future architecture of money.

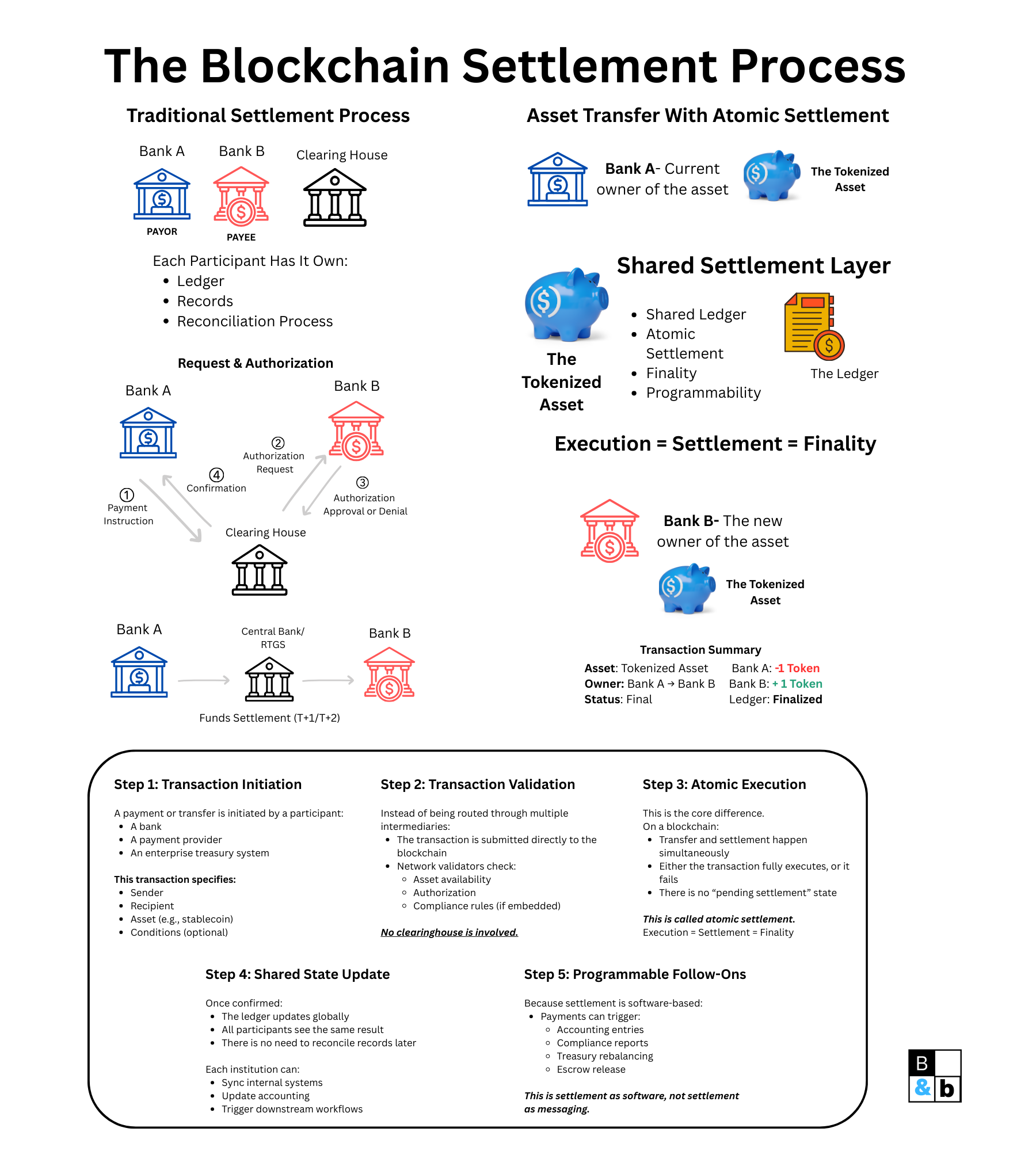

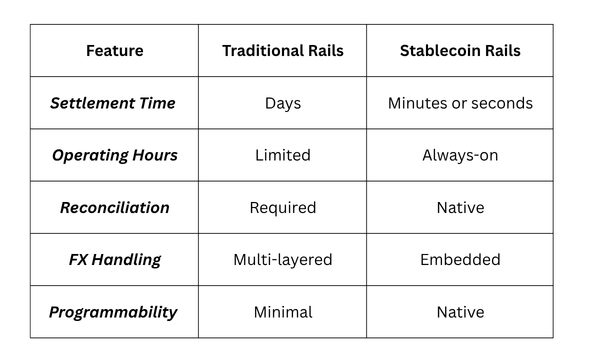

For decades, global payments have relied on layered systems built for trust, not speed. Settlement occurs through intermediated networks—banks, clearing houses, card schemes—where transactions are authorized instantly but finalized slowly. Reconciliation, batching, and counterparty risk are features, not flaws, of this design.

Stablecoins invert that model.

Instead of routing payments through networks of institutional trust, stablecoin transactions settle on shared execution layers—public blockchains—that provide finality directly at the infrastructure level. This shift is subtle but profound: money movement becomes a software process rather than an accounting one.

Public blockchains are increasingly functioning as neutral settlement networks, analogous to—but more flexible than—traditional interbank systems such as RTGS, ACH, or correspondent banking rails.

.png)

Key characteristics distinguish blockchain-based settlement:

Importantly, this does not mean blockchains replace banks. Instead, they act as interbank settlement substrates, allowing banks, issuers, and payment providers to interact on a common execution layer.

In this model, blockchains are infrastructure—not products.

As stablecoin volumes increase, settlement efficiency becomes critical. This has driven a functional division between base settlement layers (Layer 1) and execution layers optimized for throughput (Layer 2).

Layer 1 networks typically prioritize:

Layer 2 networks focus on:

For payment use cases, the distinction mirrors traditional finance:

Stablecoin systems increasingly use a hybrid approach: high-volume transactions occur on Layer 2 environments, with periodic final settlement anchored to Layer 1. This architecture supports scale without sacrificing security—an essential requirement for enterprise and bank adoption.

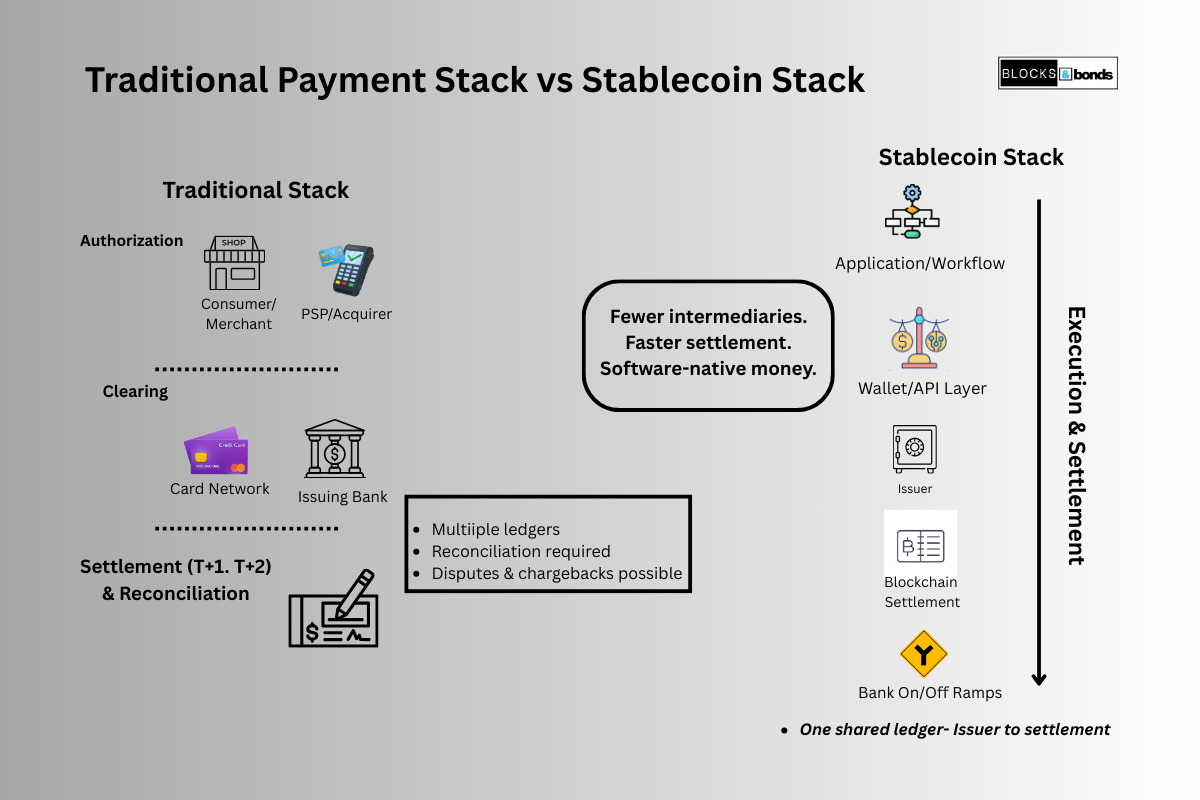

Traditional payment rails evolved to manage risk between parties who do not fully trust one another. Card networks, in particular, are optimized for consumer protection, fraud management, and dispute resolution—but at the cost of speed, transparency, and efficiency.

Stablecoin rails optimize for a different objective: final settlement.

The result is not a replacement for cards or bank transfers, but an alternative rail better suited to:

Where cards abstract settlement behind consumer convenience, stablecoins expose settlement as a programmable function.

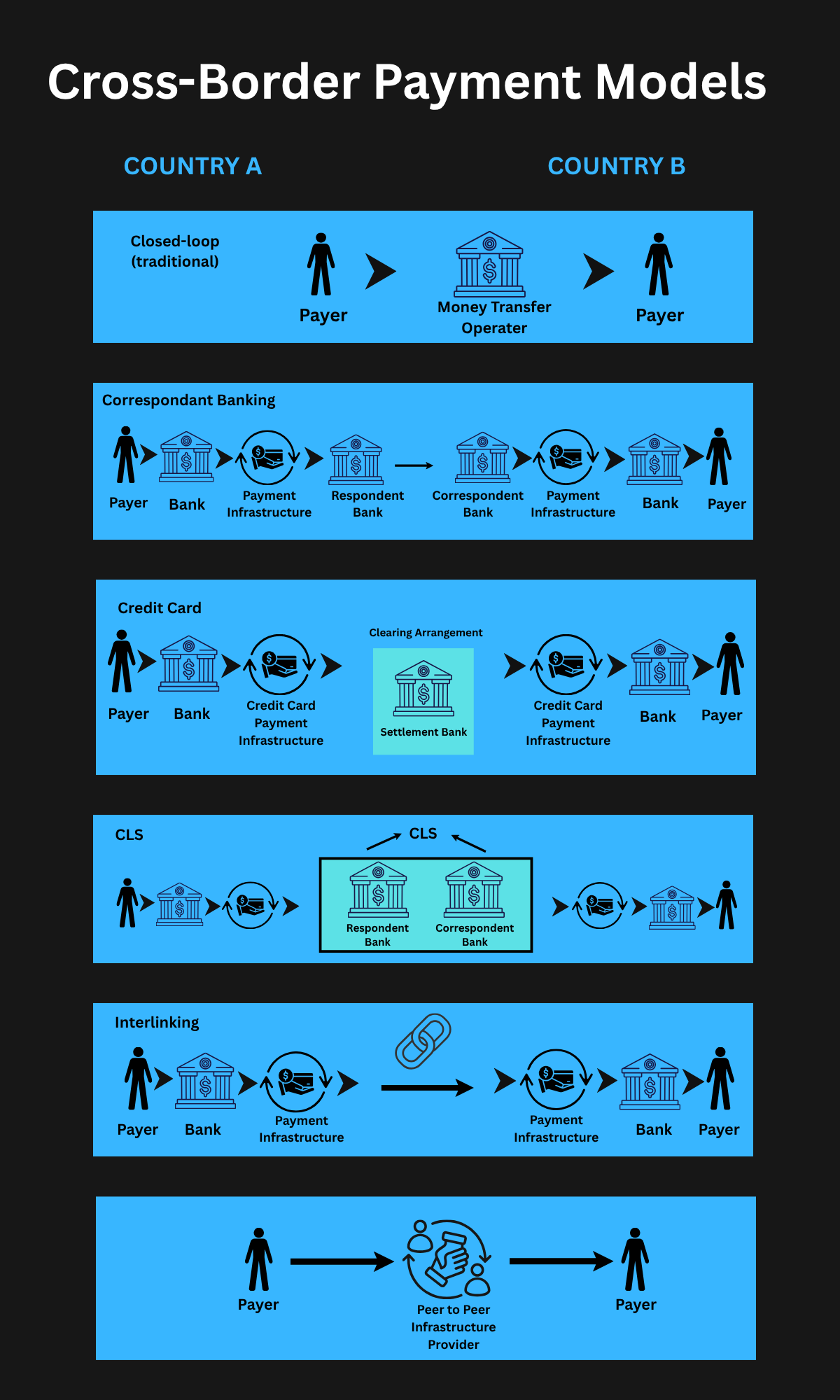

Cross-border payments are one of the clearest areas where stablecoin rails outperform legacy systems.

Traditional cross-border flows involve:

Stablecoins collapse this complexity.

By denominating transfers in a single digital settlement asset—most commonly USD-backed stablecoins—value moves directly between parties without intermediate currency conversions. FX occurs at the edge, not throughout the system.

This produces:

For enterprises operating globally, this is not a speculative advantage—it is an operational one.

The most important distinction between stablecoin rails and traditional payment systems is programmability.

Stablecoin transactions can:

This transforms settlement from a back-office function into a real-time software process.

In practice, this means:

The strategic implication is clear: the institutions that understand settlement as software—rather than as messaging—will define the next generation of payment infrastructure.

.png)

Stablecoins are not disrupting payments by competing with consumer-facing products. They are doing so by re-architecting settlement itself.

By repositioning blockchains as execution layers and stablecoins as settlement instruments, the payment stack becomes faster, simpler, and programmable. The transformation is incremental and largely invisible to end users—but foundational to the future of financial infrastructure.

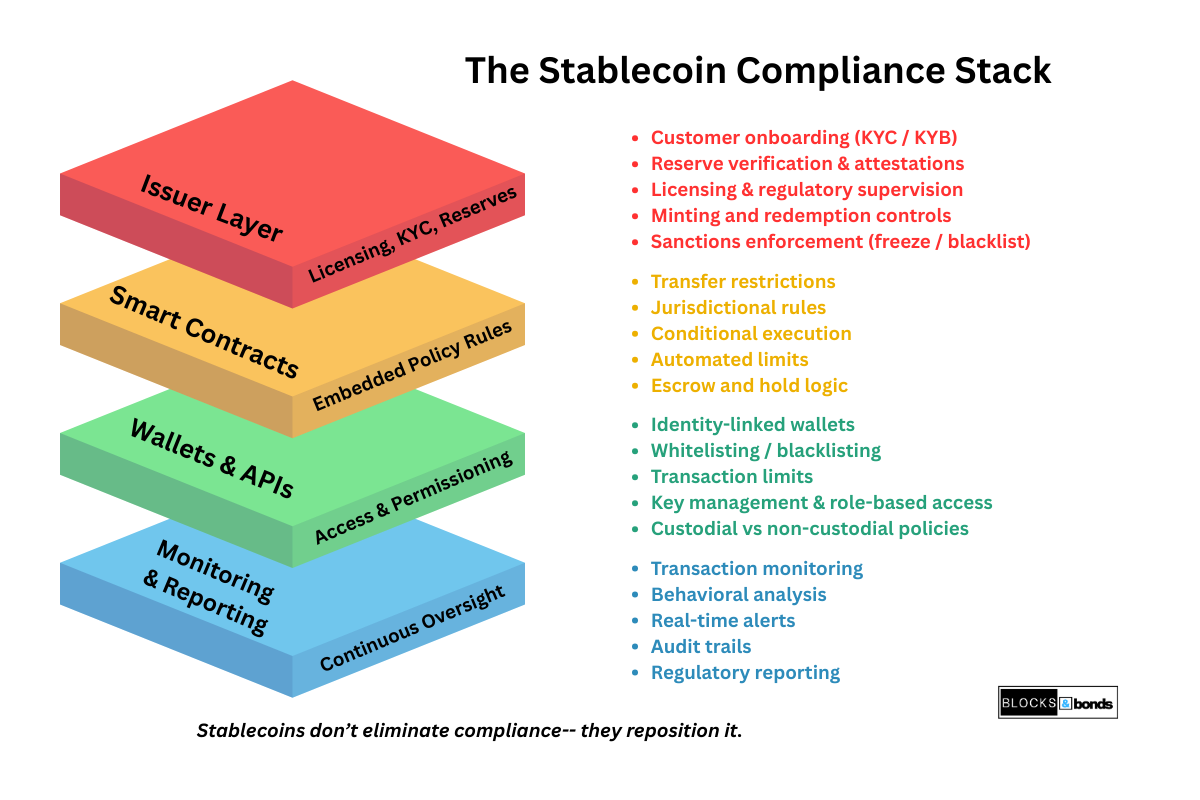

One of the most persistent misconceptions about stablecoins is that they exist outside the reach of regulation. In reality, stablecoins represent a shift not away from compliance, but toward a different compliance architecture.

Traditional financial systems embed compliance within institutions and intermediaries. Stablecoin systems embed compliance across issuers, smart contracts, wallets, and monitoring layers. Control does not disappear — it moves up and down the stack.

In payment-grade stablecoin systems, compliance is not optional or external. It is an architectural requirement.

Key compliance functions include:

These functions are increasingly standardized at the issuer level, where stablecoin providers operate under licensing regimes similar to banks or payment institutions. This centralization of responsibility allows regulators to supervise a smaller number of critical actors while maintaining visibility across the broader ecosystem.

The result is a paradoxical outcome: open networks with centralized accountability.

Stablecoin issuers sit at the center of the compliance model.

Core issuer responsibilities include:

This places issuers in a role analogous to narrow banks or regulated payment institutions. While the underlying settlement layer may be decentralized, monetary trust is anchored to the issuer.

.png)

From a regulatory perspective, this concentration simplifies oversight. From a market perspective, it creates differentiation between speculative stablecoins and payment-grade infrastructure.

Beyond issuers, compliance increasingly occurs at the wallet and service layer.

Wallet providers, custodians, and APIs implement:

This mirrors traditional financial systems, where access points — not rails — enforce policy. The difference is that stablecoin systems can enforce rules programmatically, in real time, without relying on manual intervention or post-settlement reconciliation.

For enterprises, this enables:

Smart contracts introduce a new category of financial control: programmable policy enforcement.

Examples include:

Rather than relying solely on ex-post enforcement, stablecoin systems increasingly support ex-ante compliance — rules enforced before settlement occurs.

This represents a meaningful shift:

In effect, compliance becomes software — not paperwork.

Across jurisdictions, regulatory approaches to stablecoins are converging around a shared principle: stablecoins that function like money should be regulated like payment instruments.

Common regulatory themes include:

While implementation varies by region, the broader direction is consistent. Regulators are distinguishing between:

This distinction matters. It enables compliant stablecoins to integrate with banks, payment networks, and enterprise systems — while pushing non-compliant models to the margins.

Contrary to early assumptions, regulation is not slowing stablecoin adoption. It is shaping market structure.

As compliance requirements rise:

This dynamic mirrors earlier phases of financial infrastructure development, from payment cards to electronic trading platforms. Over time, regulation does not eliminate innovation — it channels it.

For stablecoins, regulatory clarity is becoming a precondition for scale, not an obstacle to it.

Stablecoins do not represent a loss of financial control. They represent a reallocation of control across a programmable stack.

Compliance shifts:

As a result, stablecoins are evolving into policy-aware financial infrastructure — capable of meeting regulatory standards while delivering operational advantages that legacy systems cannot.

Stablecoins do not succeed by bypassing banks and enterprises. They succeed by integrating with them.

As regulatory clarity improves and settlement infrastructure matures, the center of gravity for stablecoin adoption is shifting decisively toward institutions: banks embedding stablecoins into their infrastructure, and enterprises adopting them as payment and treasury tools. This phase is not driven by ideology or experimentation, but by operational efficiency.

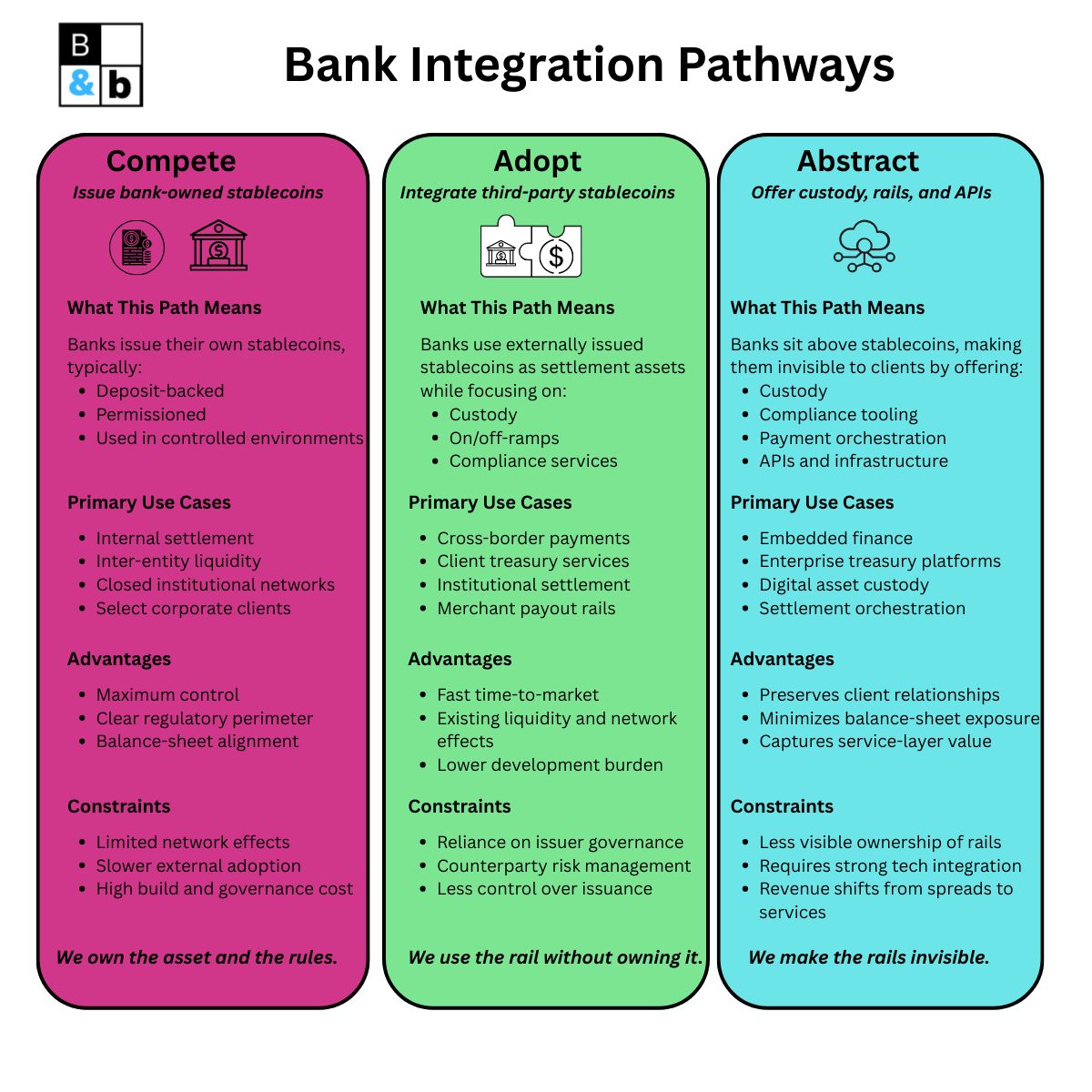

Banks face a strategic choice in how they engage with stablecoins. In practice, three integration paths are emerging.

Some banks are exploring issuing their own stablecoins, backed by deposits or segregated reserves. These instruments are typically:

This approach maximizes control but limits network effects.

Other banks integrate existing stablecoins as settlement assets, focusing on:

This model prioritizes speed to market and interoperability.

A growing number of banks are positioning themselves above the stablecoin layer, offering:

Here, stablecoins become rails — not products.

The core tension: Do banks defend deposits, or do they defend relevance?

In practice, most large institutions pursue hybrid strategies, combining elements of all three.

.png)

One of the least visible — but most impactful — use cases for stablecoins is internal bank operations.

Banks increasingly experiment with stablecoins for:

Because these flows occur behind the scenes, they attract less public attention. Yet they often deliver the strongest ROI. By reducing reconciliation complexity and enabling near-real-time settlement, stablecoins act as internal efficiency layers, not consumer-facing products.

This mirrors earlier infrastructure shifts in finance, where operational tooling preceded customer innovation.

For enterprises, stablecoin adoption is largely pragmatic.

Most businesses do not want exposure to crypto markets, token governance, or protocol risk. What they want is:

Stablecoins increasingly meet those needs.

In each case, stablecoins function as payment instruments, not speculative assets.

A critical factor in enterprise adoption is abstraction.

Stablecoins gain traction not when businesses interact directly with blockchains, but when they integrate through familiar tools:

This is why banks, fintechs, and infrastructure providers play an outsized role. They translate blockchain-native settlement into enterprise-native workflows.

The winning implementations are largely invisible:

From the enterprise perspective, the experience resembles a faster, more flexible version of existing payment rails.

Institutional adoption depends as much on governance as on technology.

Enterprises and banks evaluate stablecoin systems through familiar lenses:

As a result, adoption tends to favor:

This reinforces a broader pattern: institutional adoption concentrates around fewer, more trusted stablecoin providers.

.png)

As banks and enterprises adopt stablecoins, they exert pressure on the entire ecosystem:

This creates a feedback loop:

Over time, stablecoins evolve from optional tools into default infrastructure components for certain categories of payments.

Stablecoins are not winning adoption by appealing to consumers or displacing banks. They are doing so by solving institutional problems at the infrastructure level.

For banks, stablecoins are becoming tools for settlement, efficiency, and service expansion.

For enterprises, they are becoming faster, more flexible payment rails.

The institutions that treat stablecoins as plumbing rather than products will be best positioned to capture their long-term value.

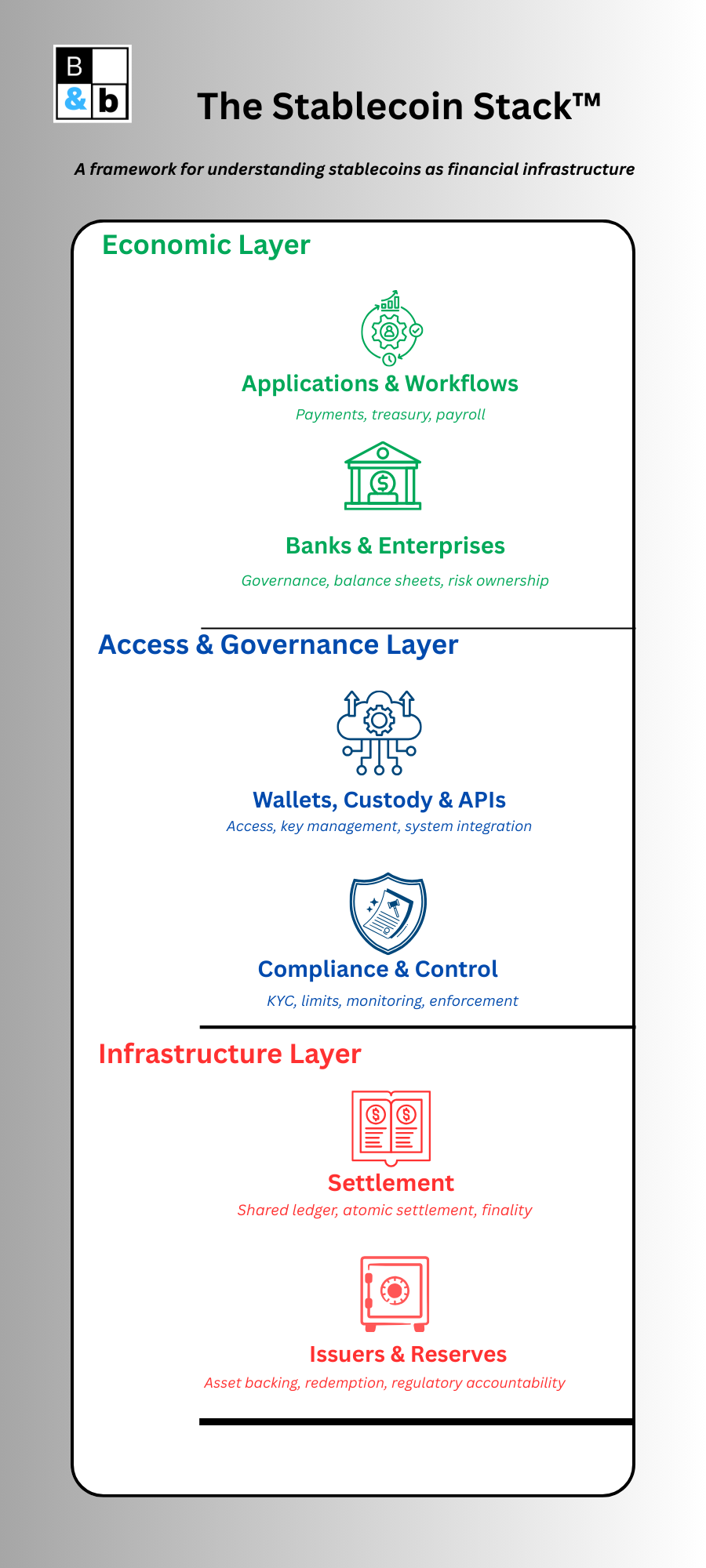

Taken individually, stablecoin issuers, blockchains, compliance tools, and bank integrations can appear fragmented. Viewed together, they form a coherent system: a new financial stack for digital settlement.

This section consolidates the report’s analysis into a single framework and outlines how that stack is likely to evolve over the next 12–36 months.

The stablecoin ecosystem is best understood as a layered stack, where each layer performs a distinct function and captures different forms of value.

1. Applications & Workflows

Payments, payroll, merchant settlement, treasury operations, embedded finance.

2. Banks & Enterprises

Custody, liquidity management, compliance oversight, and integration into existing financial operations.

3. Wallets, Custody & APIs

Secure access, transaction execution, identity controls, and system connectivity.

4. Compliance & Control

KYC/AML, sanctions screening, transaction monitoring, programmable enforcement.

5. Settlement Layer

Public or semi-public blockchains providing finality, availability, and execution.

6. Issuers & Reserves

Monetary trust, asset backing, redemption guarantees, and regulatory accountability.

This stack clarifies a key point: stablecoins are not a single product category. They are an ecosystem of interdependent services, each subject to different competitive and regulatory dynamics.

Not every layer captures value equally.

Consumer-facing applications, by contrast, are less defensible unless tightly integrated into enterprise workflows. This mirrors earlier infrastructure cycles in payments and cloud computing, where durable value accrued above and around core rails.

A growing discussion centers on tokenized bank deposits as alternatives to stablecoins. While structurally similar, the distinction is meaningful.

In practice, these models are likely to coexist. Stablecoins favor open, cross-border use cases. Tokenized deposits favor internal bank and domestic settlement. Over time, interoperability — not dominance — will define success.

.png)

Stablecoins are increasingly becoming the default settlement asset for tokenized real-world assets (RWAs), including:

As asset tokenization grows, the need for a neutral, programmable settlement instrument becomes unavoidable. Stablecoins fill this role naturally, reinforcing their position at the center of digital financial infrastructure.

Several developments are likely to define the next phase of the stablecoin stack:

For institutions, the strategic question is not whether stablecoins will persist, but where to engage in the stack.

The organizations that move early — and thoughtfully — will shape standards, capture integration advantages, and influence regulatory outcomes.

Stablecoins are not a future promise. They are already functioning as settlement infrastructure for a growing share of global value transfer.

Their impact will not be measured by consumer adoption curves or speculative cycles, but by quieter metrics:

In that sense, stablecoins resemble every major financial infrastructure shift that came before them. Transformative not because they are visible — but because, once embedded, they become indispensable.