March 1, 2026

3 minutes

May 13, 2026

5 minutes

For years, stablecoins were treated as a niche crypto product — useful mostly for traders moving between exchanges or parking funds during market volatility. That perception is changing rapidly.

Today, stablecoins are increasingly being adopted not as speculative assets, but as payment infrastructure: digital settlement rails that move money faster, cheaper, and with greater flexibility than many traditional systems.

The shift matters because payments are one of the least efficient layers of the modern financial system. Even in 2026, moving money globally often remains:

Stablecoins offer an alternative architecture.

Rather than routing transactions through layers of correspondent banks, clearing systems, and card networks, stablecoins allow value to move directly across blockchain-based networks in near real time.

The result is not simply “crypto payments.” It is the gradual rebuilding of the underlying infrastructure of money movement itself.

One of the most misunderstood aspects of stablecoins is the assumption that consumers must actively “use crypto” for the technology to matter.

In reality, much of the adoption is happening behind the scenes.

Most users may never know a stablecoin was involved in a transaction at all.

What institutions increasingly care about is infrastructure efficiency:

This is why banks, payment firms, fintech companies, and global enterprises are beginning to integrate stablecoin rails into existing systems.

The goal is not ideological decentralization.

The goal is operational efficiency.

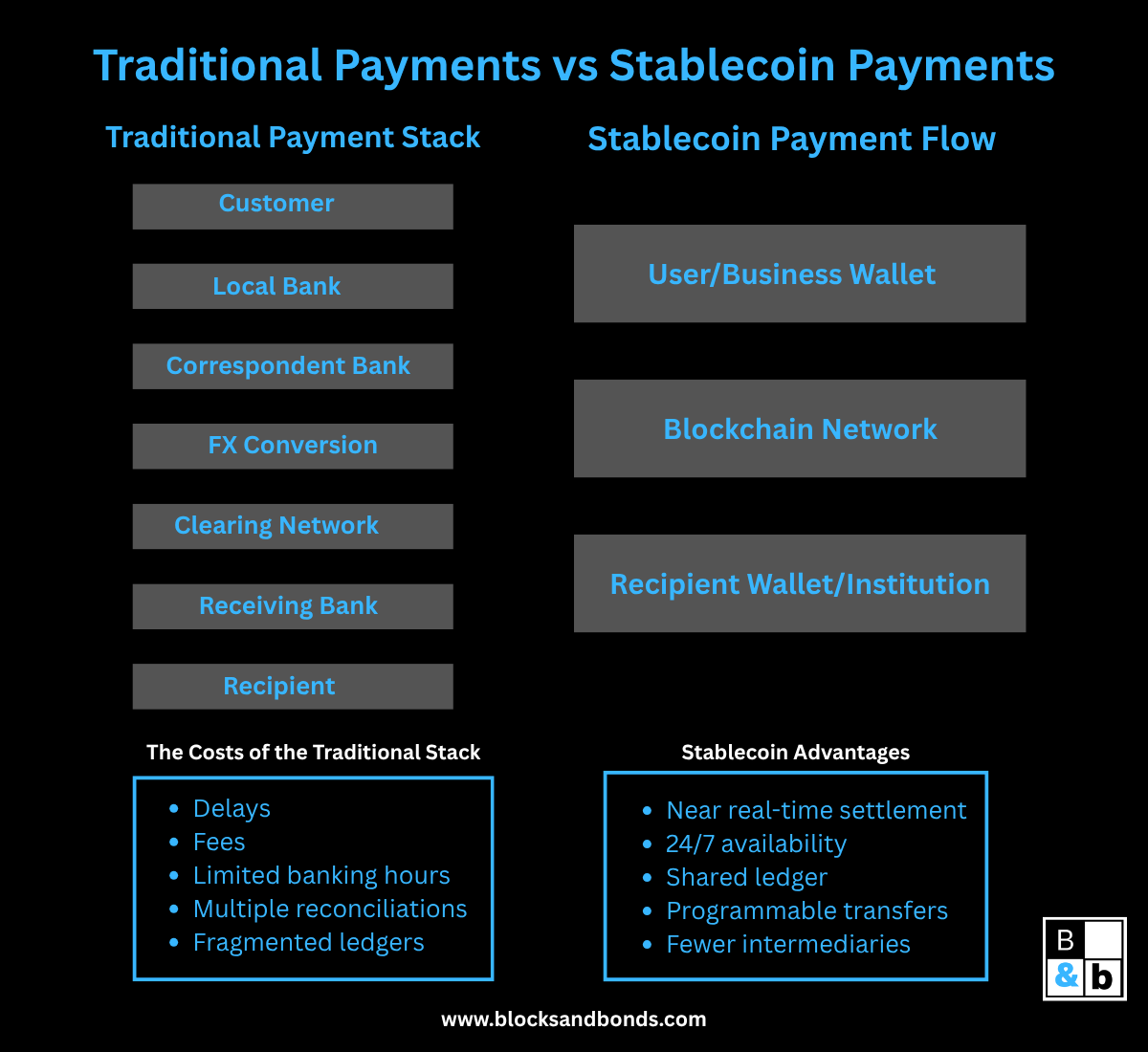

Modern payment systems were largely built in layers over decades.

Domestic payments, card networks, SWIFT messaging systems, ACH transfers, correspondent banking relationships, clearing houses, and regional settlement systems all evolved independently.

The result is a patchwork financial architecture where:

Even highly sophisticated global companies often operate with fragmented treasury systems spread across dozens of countries and banking partners.

Stablecoins simplify parts of this process by creating a shared digital settlement layer.

Instead of waiting for multiple institutions to reconcile balances across separate ledgers, transactions can settle directly on-chain with near-instant finality.

Traditional payment systems involve multiple layers:

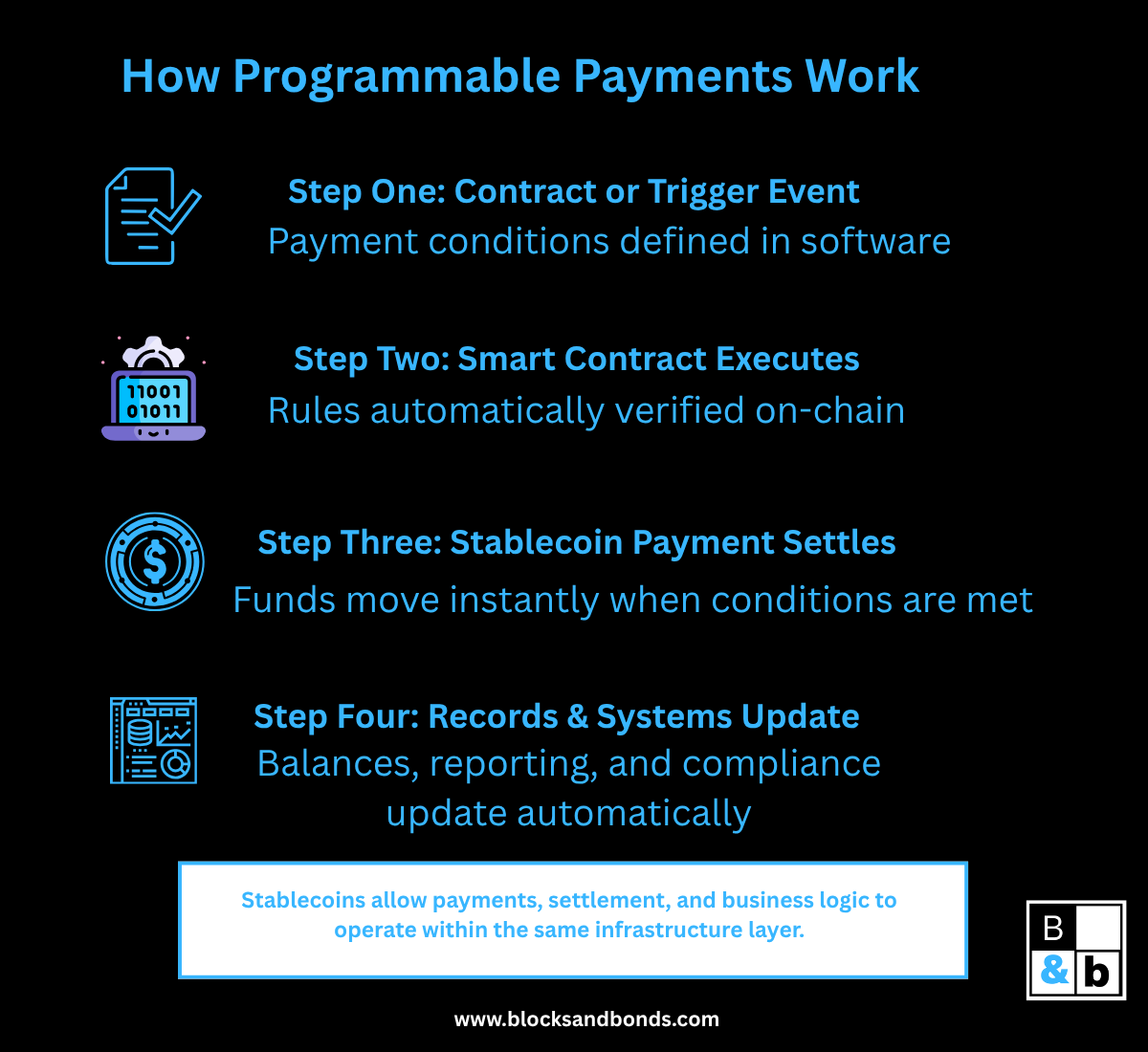

Stablecoins increasingly compress several of these layers into a single programmable system.

A transaction can:

—all within the same infrastructure environment.

This is one reason stablecoins are attracting attention from enterprise treasury departments and payment providers.

The innovation is not simply “digital dollars.”

It is the merging of payments and programmable software infrastructure.

Cross-border payments remain one of the clearest areas where stablecoins demonstrate practical advantages.

International transfers today often involve:

Stablecoin-based systems can reduce several of these frictions.

For businesses operating internationally, this can improve:

For individuals, the impact may eventually appear in:

This is particularly relevant in regions where local banking systems are slower, less accessible, or less interoperable.

One of the deeper implications of stablecoins is that payments increasingly become programmable.

Traditional payment systems typically separate:

Blockchain-based systems can combine these functions.

A payment can automatically:

This creates a financial environment where payments behave more like software systems than static banking instructions.

Over time, this may reshape:

Much of the public conversation around crypto still focuses on price volatility, speculation, or memecoins.

Meanwhile, a quieter transformation is occurring underneath the surface.

Stablecoins are increasingly becoming part of the infrastructure layer of modern finance.

Banks are experimenting with tokenized deposits.

Payment companies are exploring stablecoin settlement.

Financial institutions are integrating blockchain-based transfer systems into treasury operations.

In many cases, the end user may never directly interact with a blockchain wallet.

Instead, stablecoins may function similarly to how internet protocols operate today:

The companies that succeed in this transition may not necessarily be the ones creating the most speculative assets.

They may be the ones rebuilding the rails that move money itself.

Stablecoins are evolving from crypto trading tools into financial infrastructure.

Their significance increasingly lies not in speculation, but in their ability to improve how money moves across global systems.

The broader shift is not simply toward “digital assets.”

It is toward programmable financial infrastructure:

Whether consumers realize it or not, stablecoin rails are beginning to integrate into the next generation of payment systems.

And over time, the distinction between “traditional payments” and “crypto payments” may matter far less than the efficiency of the infrastructure beneath them.