March 1, 2026

3 minutes

Scott Kasten

March 12, 2026

5 minutes

How digital settlement infrastructure could reshape payment architecture

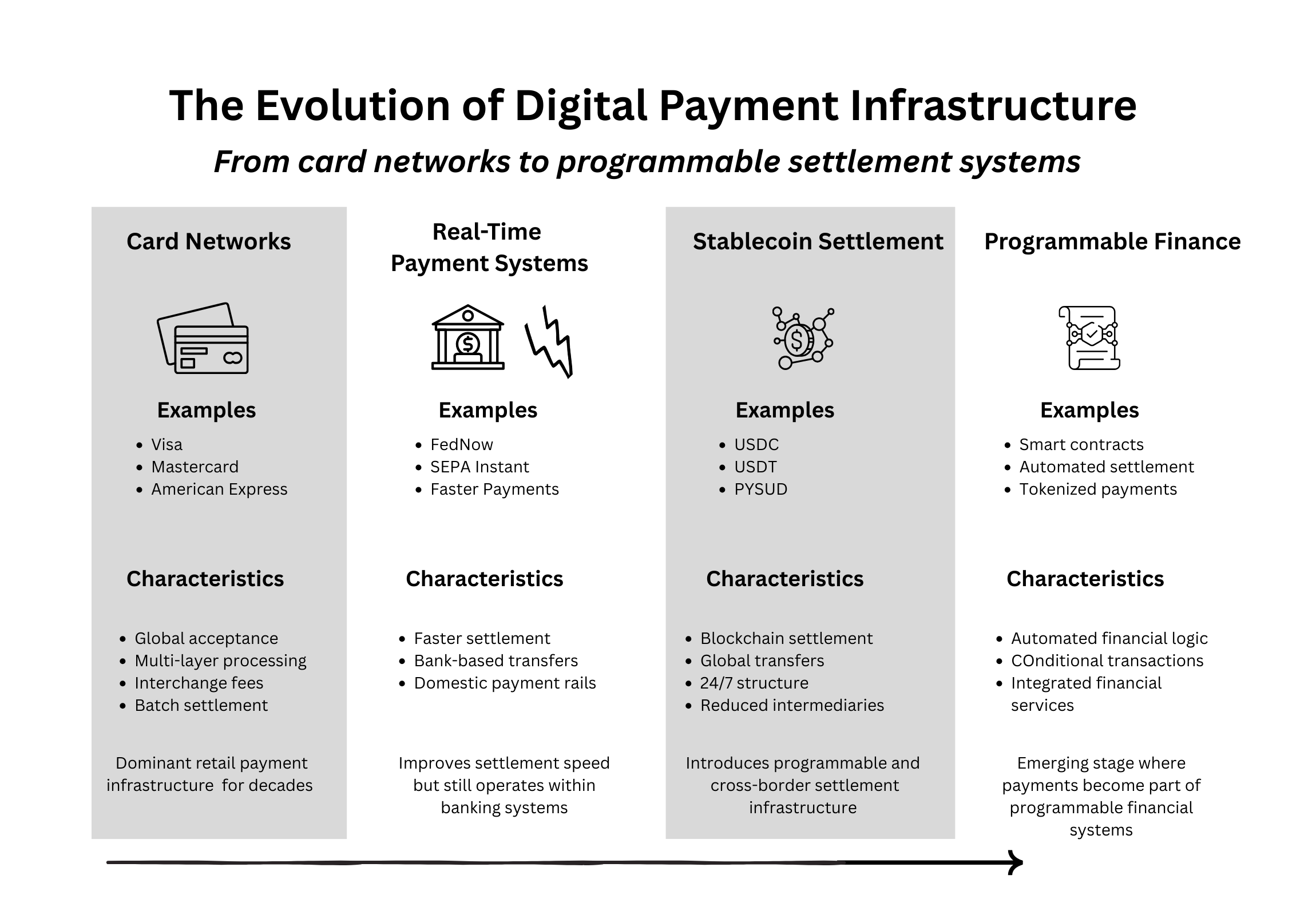

Card networks are among the most successful pieces of financial infrastructure ever built. Over the past half century, networks such as Visa and Mastercard have created a global system connecting banks, merchants, payment processors, and consumers. These systems process trillions of dollars in transactions each year and form the backbone of modern electronic commerce.

Stablecoins introduce a different architectural model for digital payments. Rather than routing transactions through multiple layers of financial intermediaries, stablecoin transactions can move directly between digital wallets on blockchain networks. In principle, settlement occurs at the infrastructure layer itself.

This difference does not imply that stablecoins will replace card networks in the near term. Card systems provide valuable services such as fraud protection, dispute resolution, and merchant integration that blockchain networks do not easily replicate. But stablecoins do introduce an alternative settlement architecture that could reshape parts of the payments ecosystem over time.

Understanding the relationship between these two systems requires looking beyond consumer payments and focusing on the underlying infrastructure of financial settlement.

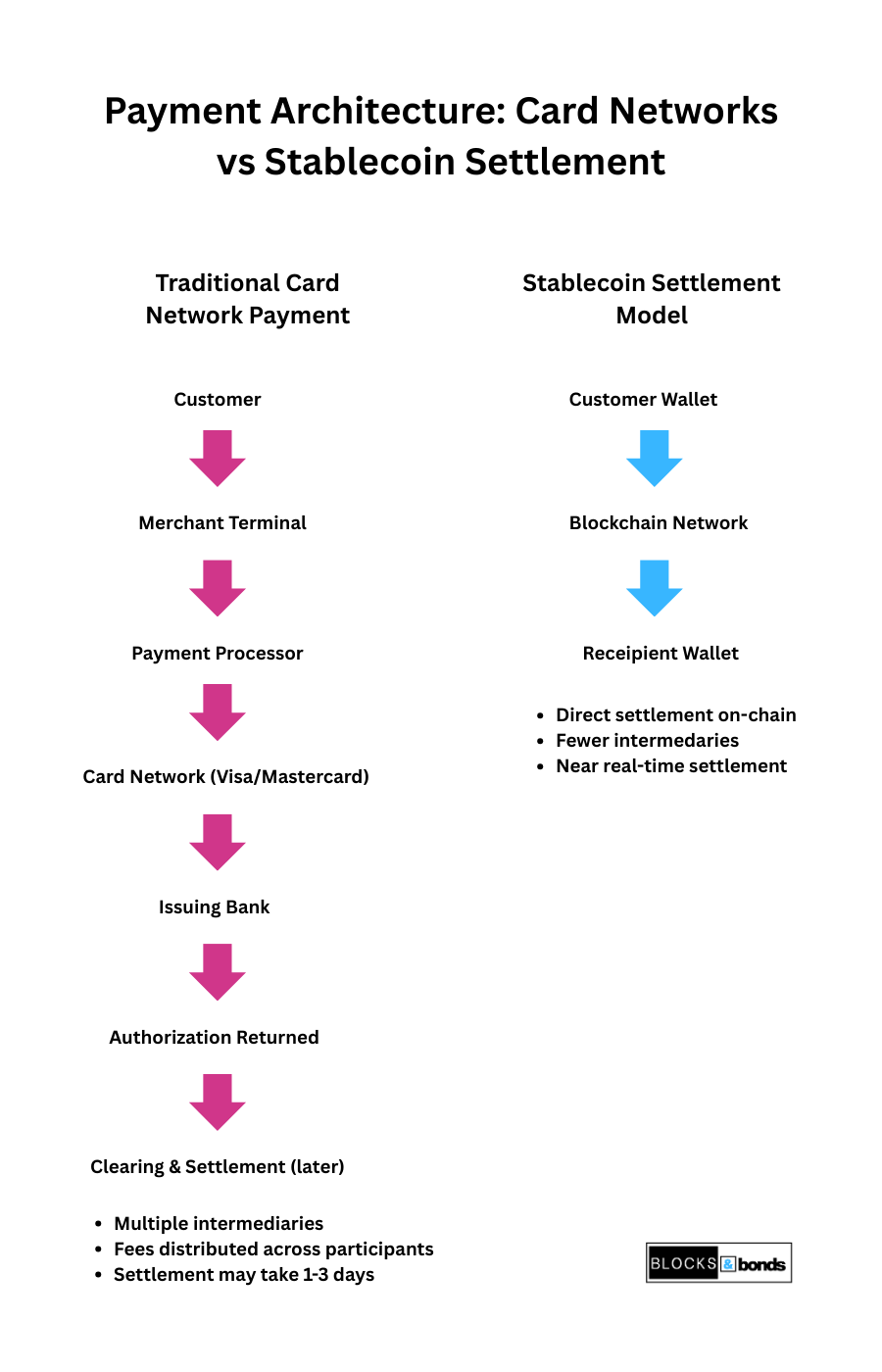

Card payments appear simple to consumers. A customer swipes a card, and the transaction is approved within seconds. Behind the scenes, however, the process involves several layers of financial infrastructure.

A typical card transaction includes:

This architecture evolved to solve a range of challenges: fraud management, credit risk, regulatory compliance, and merchant integration. The result is a highly reliable system that can process enormous volumes of payments.

However, this infrastructure also introduces multiple intermediaries and transaction fees. Merchants typically pay interchange and processing costs, and cross-border payments may involve additional currency conversion and settlement delays.

The system works well for retail commerce, but its complexity reflects the constraints of legacy financial infrastructure.

Stablecoins approach payments from a different starting point, operating on blockchain settlement infrastructure that differs from traditional financial systems. (See our analysis of on-chain vs off-chain settlement.) Instead of routing transactions through several banking and network intermediaries, stablecoin payments can occur directly between digital wallets on blockchain networks.

In its simplest form, the payment flow becomes:

wallet → blockchain network → recipient wallet

Settlement occurs when the transaction is confirmed on the underlying blockchain.

This architecture compresses several layers of the traditional payment stack. Instead of clearing and settlement occurring across multiple institutions, the blockchain itself functions as the settlement layer.

The result can be faster transaction finality and lower operational friction, particularly in contexts where traditional payment systems are inefficient.

Stablecoins are unlikely to immediately disrupt consumer card payments in developed markets. Card networks offer a mature ecosystem that includes merchant integration, credit services, and dispute resolution mechanisms.

However, stablecoins may prove competitive in areas where the traditional payment infrastructure is less efficient.

Three areas stand out.

International payments often require multiple correspondent banking relationships and can take several days to settle. Stablecoin transfers can move value across borders in minutes, reducing settlement delays and operational complexity.

Online platforms increasingly operate across jurisdictions and currencies. Stablecoins provide a standardized digital settlement asset that can simplify payment flows for global digital businesses.

Because stablecoins operate on programmable blockchain networks, they can support automated payments, conditional transfers, and integrated financial logic. These capabilities may be particularly useful in areas such as decentralized finance and digital asset markets.

Despite these advantages, stablecoins do not eliminate the functions provided by card networks.

Card systems offer:

These services represent decades of institutional development. Replicating them purely through blockchain systems would be difficult.

For this reason, the most likely near-term outcome is integration rather than direct competition. Stablecoins may increasingly function as settlement rails beneath payment applications, while traditional financial institutions continue to provide consumer-facing services.

Some payment companies and fintech platforms are already experimenting with this model, combining blockchain settlement with existing financial infrastructure.

For financial institutions and payment companies, stablecoins represent less a new form of consumer payment and more a potential evolution in settlement infrastructure.

Banks may explore stablecoins as tools for:

Payment companies may experiment with stablecoins as a way to reduce friction in global payment flows.

In both cases, the impact of stablecoins will depend less on consumer adoption and more on how effectively they integrate with existing financial systems.

Card networks remain one of the most effective payment systems ever created. Their global acceptance, consumer protections, and operational reliability make them difficult to replace.

Stablecoins, however, introduce a different model for moving value. By enabling direct settlement on blockchain networks, they compress several layers of the traditional payment stack and create new possibilities for global financial infrastructure.

Rather than immediately replacing card networks, stablecoins may gradually reshape parts of the payments ecosystem—particularly where traditional settlement systems are slow, complex, or costly.

The most significant impact of stablecoins may therefore occur not at the consumer checkout counter, but deeper within the infrastructure that moves money around the global financial system.