April 26, 2026

4 minutes

July 13, 2026

11 minutes

Why adoption, usage, and technological importance do not always translate into value for token holders.

Crypto markets often assume that if a technology becomes important, the token associated with it must become valuable.

The relationship is rarely that simple.

A blockchain can process more transactions without delivering equivalent value to its token holders. A stablecoin can become widely used while most of the resulting economics accrue to its issuer. A tokenized fund can attract billions of dollars while the asset manager, custodian, transfer agent, and distribution platform capture more value than the blockchain carrying the product.

Usefulness matters. Adoption matters. Transaction volume matters.

But none of them answer the central economic question:

Who gets paid?

That question sits at the heart of value-accrual analysis.

As digital assets move from speculative narratives toward financial infrastructure, investors and institutions need to look beyond whether a system is growing. They need to understand which layer controls the customer relationship, collects fees, earns interest, directs liquidity, owns the data, or becomes difficult to replace.

The crypto stack may be decentralized in design, but its economics are not evenly distributed.

A technology can become widely used without producing strong returns for every participant connected to it.

The internet created enormous economic value, but that value did not accrue equally to internet service providers, hardware manufacturers, websites, software companies, marketplaces, and end users. Some layers became highly profitable. Others became commoditized.

Cloud computing followed a similar pattern. Thousands of companies benefited from cloud infrastructure, but a relatively small number of providers captured a large share of the economic value.

Digital assets are likely to develop in the same way.

The growth of blockchain-based finance may create value across the economy while concentrating profits in a limited number of layers. Some networks may become essential but inexpensive utilities. Some applications may own the customer relationship. Some intermediaries may earn durable fees because regulation, trust, or operational complexity makes them difficult to replace.

This means technological importance and investment value must be analyzed separately.

A system can matter enormously without its token being a strong investment.

The simplest way to understand value accrual is to follow the money.

Where does revenue enter the system?

Who pays it?

Why are they willing to pay?

Who collects it?

What costs must be covered before any economic value reaches investors or token holders?

These questions cut through many of the abstractions that make crypto markets difficult to evaluate.

A protocol may report high transaction volume, but volume alone does not reveal whether users are paying meaningful fees. A network may collect fees, but those fees may be distributed to validators rather than token holders. A platform may generate revenue, but most of it may be spent on incentives intended to attract users and liquidity.

The existence of activity is not enough.

Value accrues when activity creates durable economic benefits that can be retained by a particular participant in the system.

That participant might be a token holder. It might also be a company, issuer, validator, asset manager, exchange, market maker, custodian, or software provider.

The crypto economy can be understood as a set of connected layers. Each performs a different function, and each has a different mechanism for capturing value.

Settlement networks include the blockchains on which transactions are recorded and finalized.

Their economic role is fundamental. They provide the shared ledger, transaction ordering, security, and finality that allow digital assets and applications to operate.

Settlement networks may capture value through transaction fees, demand for their native asset, validator economics, and the use of the native token as collateral or a reserve asset within the ecosystem.

But high usage does not automatically create strong token value.

Fees may remain low because block space is abundant. Layer-two systems may reduce the amount users pay directly to the underlying network. Competition may force transaction costs downward. Applications may capture the customer relationship while treating the underlying blockchain as interchangeable infrastructure.

The key question is whether the network possesses something difficult to replace: trusted security, deep liquidity, strong developer activity, established distribution, or a role as the preferred settlement asset.

Without those advantages, settlement can become a commodity.

Scaling systems process transactions more efficiently and often settle their results to another blockchain.

They can improve speed, lower costs, and make blockchain applications practical for larger numbers of users.

Their value may come from transaction fees, sequencer revenue, interoperability, application distribution, or control over the environment in which developers build.

But the economics can be complicated.

A scaling network may generate substantial activity while paying part of its revenue to the underlying settlement layer. It may need to subsidize users, developers, or liquidity providers. Its token may be used primarily for governance without receiving a direct share of the economics.

Investors therefore need to separate three questions:

Those are not the same question.

Stablecoins can capture value in a particularly direct way.

An issuer receives conventional assets in exchange for digital tokens. The reserves may be held in cash, Treasury bills, money market instruments, or similar assets. The issuer can earn income on those reserves while users hold and transfer the stablecoin.

That creates a potentially powerful business model: the issuer earns revenue from the reserve portfolio while users benefit from the stablecoin’s liquidity, transferability, and integration into digital applications.

Value can also accrue to exchanges, wallets, payment processors, banks, and fintech platforms that distribute the stablecoin or connect it to customers.

The blockchain carrying the stablecoin may benefit from transaction activity, but it does not necessarily capture most of the economics. The stablecoin issuer may earn the reserve income. The wallet may control the customer. The payment platform may charge the service fee.

The largest value pool may therefore sit above the settlement network.

Applications are where users borrow, trade, invest, transfer money, manage assets, or interact with tokenized products.

These businesses and protocols are often closest to the customer and the actual financial activity.

They may capture value through trading fees, lending spreads, management fees, subscription charges, issuance fees, servicing revenue, or a percentage of assets under management.

This proximity to users can create strong economics. Applications can develop recognizable brands, specialized data, integrated workflows, and customer relationships that are harder to replace than the underlying technology.

But applications face their own risks.

They may operate in competitive markets with low switching costs. Their code may be copied. Users may move quickly when incentives change. Regulatory obligations may raise costs. Revenue may depend heavily on speculative trading rather than recurring economic activity.

An application creates durable value when users return because it performs an important function—not simply because it is paying them to remain.

Some of the most durable value may accrue to businesses that solve the least glamorous problems.

Institutions require secure custody, key management, transaction monitoring, identity verification, sanctions screening, reporting, auditing, insurance, governance controls, and cybersecurity.

These functions do not usually generate the same public excitement as new tokens or trading applications. But they can become difficult to replace because they sit at the intersection of technology, regulation, trust, and institutional operations.

A bank or asset manager may be willing to change blockchains. It will be less willing to replace a deeply integrated custody or compliance provider without a compelling reason.

That creates the possibility of sticky revenue and high switching costs.

The more digital assets become part of conventional finance, the more value may migrate toward the companies that make the systems safe, compliant, and operationally usable.

Tokenization creates another important distinction between technological activity and economic capture.

A tokenized Treasury fund may use a blockchain for recordkeeping and transfers, but the blockchain is only one component of the product.

The asset manager may earn a management fee. The custodian may earn a custody fee. The tokenization platform may charge for issuance and administration. A distributor may control access to investors. A transfer agent or compliance provider may oversee ownership records and transfer restrictions.

The blockchain may receive only a small transaction fee.

This does not make the blockchain unimportant. It means the economics of the product are distributed across several layers, and the most visible layer is not always the most profitable.

Tokenization should therefore be analyzed as a complete financial product rather than a token placed on a ledger.

Markets cannot function without liquidity.

Exchanges connect buyers and sellers. Market makers provide prices and inventory. Brokers, custodians, and settlement providers help institutions execute and complete transactions.

These participants may capture value through trading fees, spreads, financing, custody charges, listing fees, or access to order flow.

Their importance often increases as a market becomes more institutional.

Large investors care not only whether an asset exists, but whether it can be bought, sold, financed, held, and valued at scale. A technically sound tokenized asset with little liquidity remains of limited use to many institutions.

The entities that organize liquidity can therefore become major economic beneficiaries even when they did not create the underlying asset or network.

One of the largest analytical mistakes in digital asset markets is treating all tokens as though they function like shares in a company.

They do not.

A token may be used to pay transaction fees. It may secure a network through staking. It may provide governance rights. It may offer access to a service. It may serve as collateral. It may be used to distribute incentives.

None of those functions automatically gives the holder a legal or economic claim on revenue.

A company’s shareholders may possess a recognized residual claim on the value of the business. A token holder may have no comparable right to cash flow, assets, or distributions.

This does not mean the token has no value. Demand can arise from utility, scarcity, collateral use, network security, or the need to hold the asset to participate in the system.

But investors need to identify the actual mechanism.

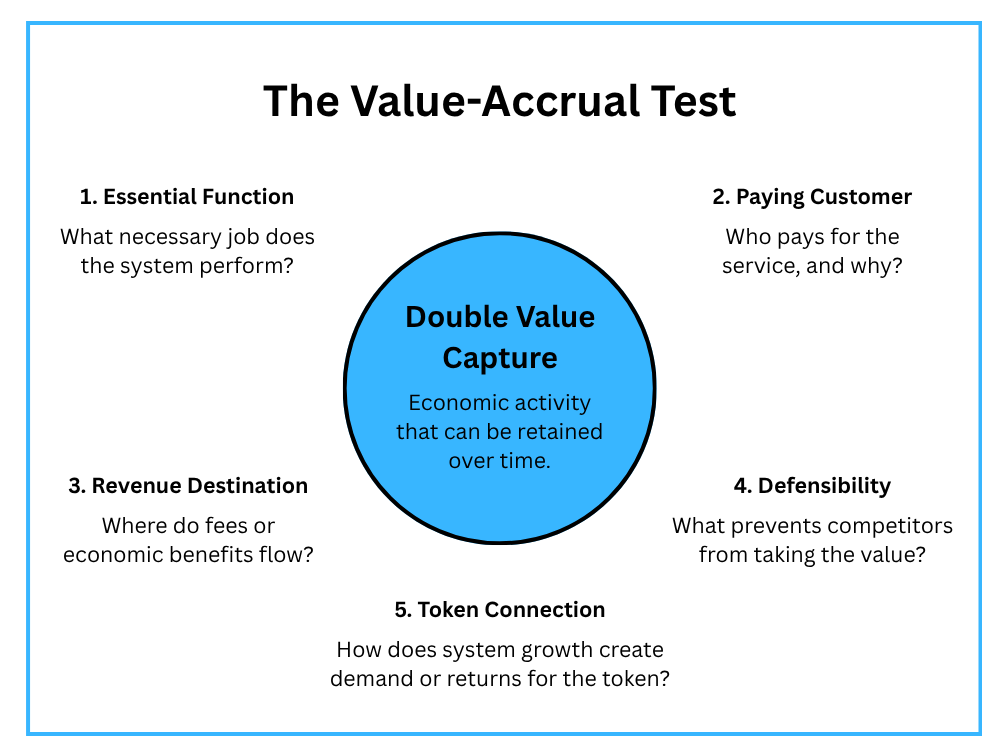

A strong value-accrual model should answer:

Without a clear answer, the link between adoption and token value may be largely narrative.

Even where revenue exists, it does not always become durable value.

A system may generate fees while spending heavily on token incentives. Revenue may depend on unusually high market volatility. A platform may offer unsustainably high yields to attract deposits. A protocol may distribute nearly all of its economics to liquidity providers, validators, or users.

Investors therefore need to distinguish between gross activity and retained value.

The more useful questions are:

A protocol with modest but recurring revenue may be more valuable than one with enormous but temporary volume.

Durability matters more than spectacle.

Value often concentrates at choke points: parts of the system that other participants must pass through and cannot easily replace.

A choke point might be a trusted settlement asset, a dominant custody platform, a widely integrated stablecoin, a liquidity venue, a regulatory license, a compliance network, or a source of essential data.

The strongest choke points usually possess one or more of the following:

These advantages make it possible to retain more of the value generated by the wider ecosystem.

The most important layer is therefore not always the one with the most advanced technology. It may be the layer that controls access, trust, liquidity, or distribution.

As the digital asset market matures, value is likely to concentrate in several places.

Settlement networks with credible security and persistent demand may retain significant value. Stablecoin issuers may benefit from reserve income and distribution. Asset managers may earn fees from tokenized financial products. Custody and compliance providers may become embedded in institutional workflows. Exchanges and market makers may capture the economics of liquidity. Applications may benefit from direct customer relationships and recurring financial activity.

At the same time, other layers may become commoditized.

Transaction processing may become cheaper. Blockchains may compete aggressively for applications. Similar protocols may offer interchangeable services. Open-source software may reduce barriers to entry. Token incentives may temporarily disguise weak customer loyalty.

This means the crypto stack will not produce one winner or one universal model of value accrual.

Different layers will capture value for different reasons.

The task is to identify which advantages are structural and which are temporary.

A useful value-accrual analysis can be reduced to five questions.

Does it settle transactions, provide liquidity, issue an asset, secure ownership, manage risk, or connect users to a financial service?

Are the customers traders, institutions, developers, asset managers, businesses, or consumers?

Does it reach a company, validators, token holders, liquidity providers, or several groups at once?

Look for switching costs, network effects, regulation, trusted distribution, proprietary technology, or control over liquidity.

Determine whether the token has a necessary and durable role—or whether it sits beside a successful system without capturing its value.

At the center of the framework is a simple distinction:

Value creation describes what the system contributes. Value capture describes who keeps the economic benefit.

Crypto markets are good at identifying what is new.

They are less consistent at identifying who will benefit when the new technology becomes ordinary.

The loudest project may not control the customer relationship. The busiest blockchain may not retain the largest share of the economics. The most widely used token may not give its holders a claim on the revenue it helps create.

As digital asset markets mature, these distinctions will become harder to ignore.

The winners will not simply be the projects generating activity. They will be the networks, companies, issuers, applications, and infrastructure providers capable of converting activity into durable economic advantage.

That requires more than attention.

It requires revenue, defensibility, integration, trust, and a credible mechanism for retaining value.

The central question is therefore not simply whether crypto infrastructure will grow.

It is where, within that infrastructure, the value will remain.