April 26, 2026

9 minutes

July 13, 2026

13 minutes

Why the next phase of digital assets will be judged less by speculation and more by market structure, settlement, custody, compliance, and institutional utility.

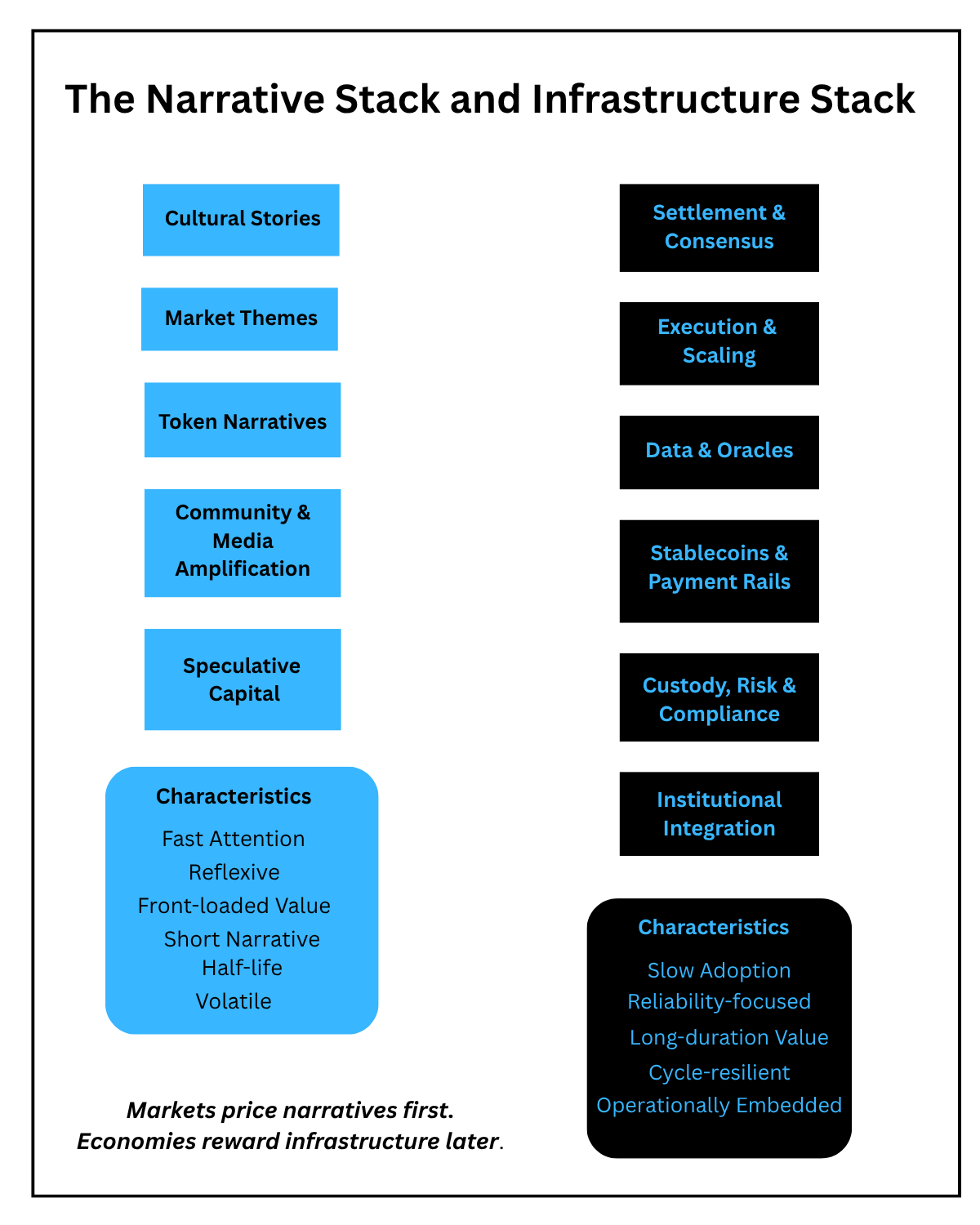

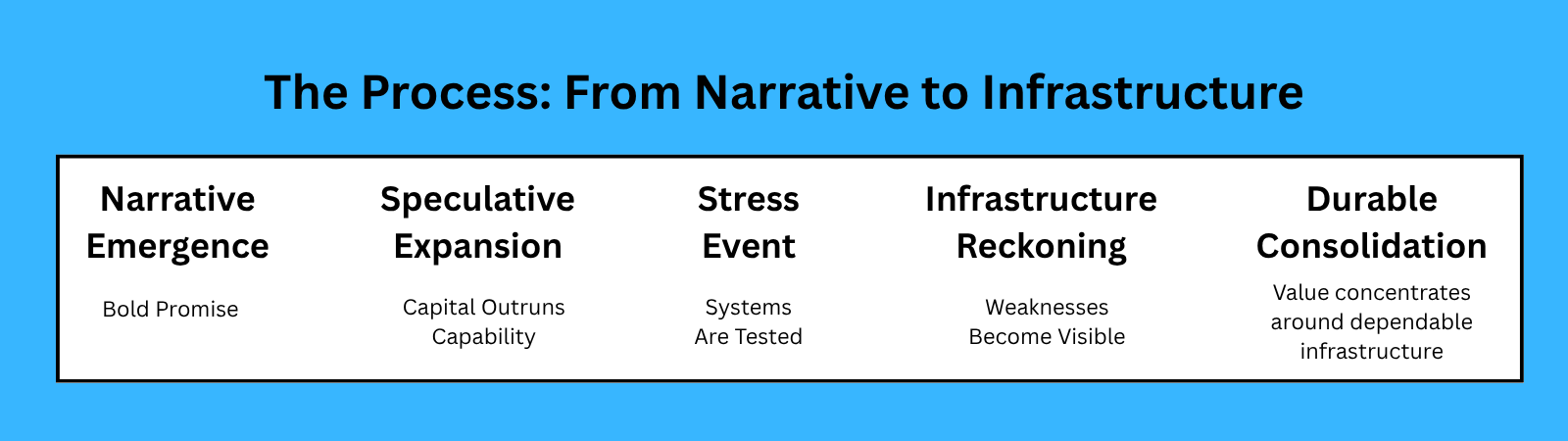

This is the core thesis behind Blocks & Bonds: digital assets are moving from narrative markets to infrastructure markets.

For most of crypto’s public life, the industry has been explained through stories.

Bitcoin was digital gold. Ethereum was the world computer. DeFi was the future of finance. NFTs represented digital ownership. DAOs would reinvent organizations. Stablecoins were crypto’s dollar layer. Tokenization would place the world’s assets on-chain.

These narratives mattered. They gave complex technologies a recognizable purpose. They attracted capital, talent, experimentation, and public attention long before the underlying systems were mature enough to support widespread use.

Some of those narratives were directionally correct. Some were premature. Others were little more than marketing language dressed up as strategy. But together they shaped how investors, builders, regulators, institutions, and the public understood digital assets.

The problem is that narratives can outrun infrastructure.

A compelling story can attract users and capital before a system has solved the difficult questions beneath it: how value is settled, how assets are held, how ownership is enforced, how liquidity forms, how risks are managed, and what happens when the system fails.

Crypto is now entering the phase in which those questions matter more than the slogans.

The central issue is no longer whether digital assets can generate attention. They can. The question is whether blockchain-based systems can become useful, trusted, compliant, liquid, resilient, and economically superior financial infrastructure.

That is the lens behind Blocks & Bonds.

Blocks & Bonds is built around a simple editorial distinction: we are less interested in crypto as a recurring cycle of hype than in digital assets as an emerging layer of financial infrastructure.

That means paying close attention to stablecoins, tokenized assets, custody, settlement, compliance, liquidity, market structure, regulation, and institutional adoption.

These are not secondary subjects that become relevant after the technology has succeeded. They are the conditions that determine whether it succeeds.

This article explains the framework we use across our research.

The history of crypto is filled with moments when a powerful narrative collided with an incomplete system.

Tokens launched before the networks beneath them could scale. Decentralized organizations formed before their governance mechanisms had been tested under pressure. DeFi protocols accumulated billions of dollars before risk management, oracle design, and smart-contract security had matured. Tokens were marketed as ownership instruments even when the legal rights attached to them remained unclear.

The language moved faster than the architecture.

This pattern is not unique to digital assets. Railroads, electricity, telecommunications, the internet, mobile computing, and cloud infrastructure all passed through periods in which expectations advanced faster than practical capability.

New technologies are often introduced to the public through promises. Their durable economic value appears later, after standards are established, failures are absorbed, business models are refined, and the underlying infrastructure becomes dependable enough to fade into the background.

Crypto is beginning to face the same transition.

The industry does not lack ideas. It lacks enough systems capable of surviving contact with law, regulation, accounting, custody, cybersecurity, institutional operations, and real-world risk.

That is the divide between a narrative market and an infrastructure market.

The first phase of crypto was defined primarily by assets.

Tokens traded. Prices moved. Exchanges expanded. New networks launched. Retail investors entered and exited. Financial media interpreted the market through volatility, scandals, personalities, and repeating cycles of boom and contraction.

That phase was not meaningless. It created liquidity, experimentation, technical talent, and public awareness. It also produced the economic incentives that financed much of the infrastructure now being developed.

But it distorted the larger conversation.

When an ecosystem is viewed primarily through token prices, volatility can be mistaken for importance. Market capitalization becomes a proxy for usefulness. Attention becomes confused with adoption.

The deeper possibility is not merely that crypto has created a new class of speculative assets. It is that blockchains may become part of the infrastructure through which financial claims are issued, transferred, settled, secured, administered, and governed.

An asset-class narrative asks whether a token will appreciate.

An infrastructure analysis asks what function a system performs, who depends on it, what costs it changes, what risks it reduces or introduces, what legal rights it represents, and whether it can operate across institutions, jurisdictions, and market cycles.

It also asks a more difficult question: what happens when it fails?

Those questions are less exciting than price forecasts. They are also the questions that determine whether a technology can become part of the financial system.

Narratives are effective because they simplify complexity. They give investors and users a reason to participate before the practical value of a new system is fully visible.

But narrative-driven markets eventually encounter three limits.

First, narratives become saturated. When every network claims to be faster, more scalable, more decentralized, and more community-owned, the language loses its ability to distinguish one project from another.

Second, narratives are volatile. They depend on social consensus, abundant liquidity, and continuing attention. When market conditions change or a prominent failure occurs, belief can unwind faster than infrastructure can prove its value.

Third, narrative-reality gaps become harder to ignore. Institutions, regulators, and serious users eventually compare what a technology promised with what it reliably delivers.

A protocol may claim to eliminate intermediaries while depending on wallets, bridges, exchanges, market makers, oracle providers, custodians, auditors, and governance delegates. A token may appear to represent ownership while the actual claim remains embedded in contracts, issuer records, custodial arrangements, or off-chain legal entities.

This does not mean the original ideas were empty.

DeFi demonstrated the potential of programmable financial logic. Stablecoins proved that dollar-denominated value could circulate across blockchain networks. NFTs showed how digital scarcity could be coordinated through shared ledgers. DAOs experimented with new forms of collective decision-making. Tokenization demonstrated that conventional financial claims could be represented and administered through programmable systems.

But an experiment is not yet infrastructure.

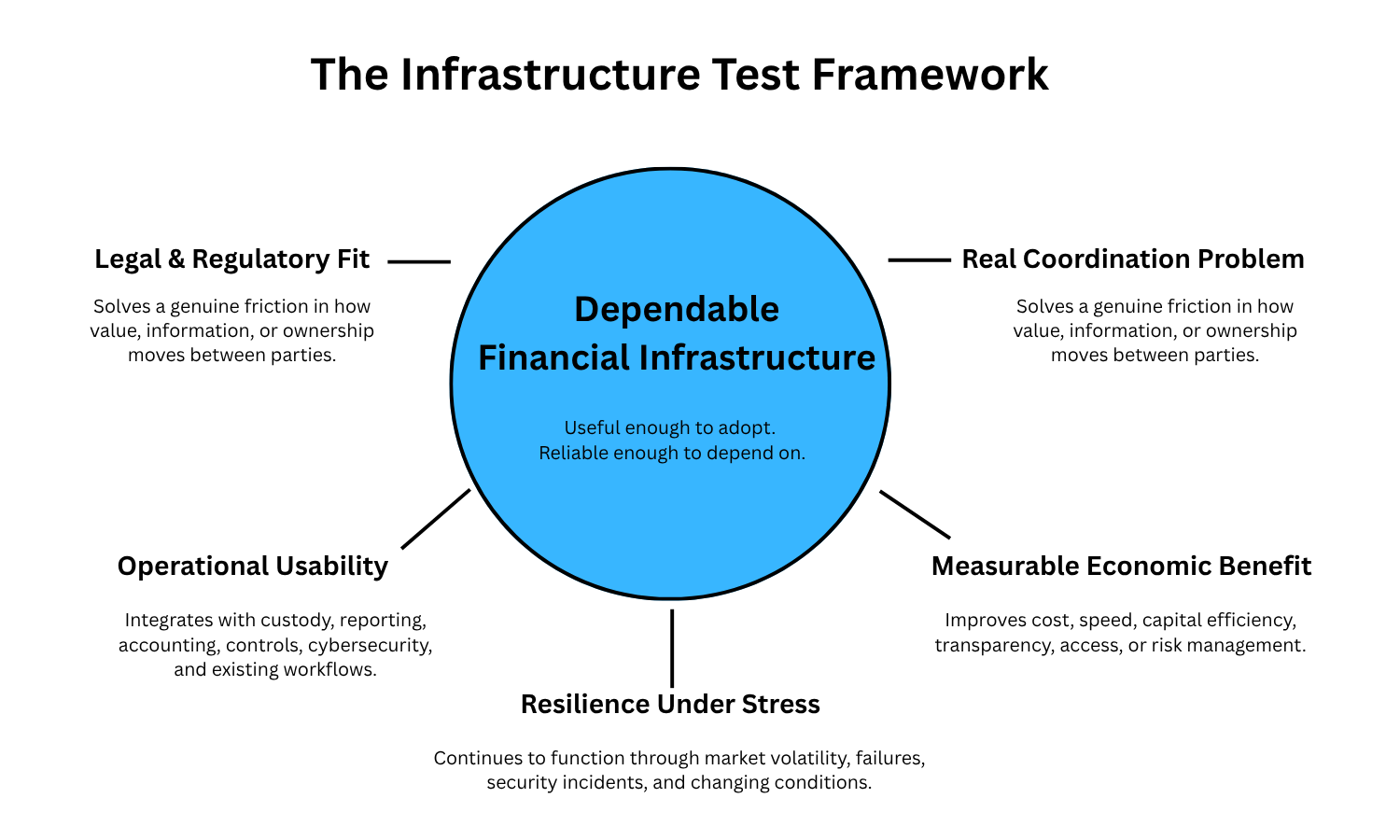

Infrastructure begins when the market stops asking whether a concept is possible and begins asking whether it is dependable.

A digital asset system becomes strategically important when it passes several tests at the same time.

It must solve a genuine coordination problem. That problem might involve slow settlement, fragmented liquidity, expensive cross-border payments, inefficient collateral movement, opaque ownership records, limited asset access, or complex reconciliation among institutions.

It must produce a measurable economic benefit. The improvement should appear in settlement time, operating costs, capital efficiency, compliance automation, distribution, liquidity, transparency, or risk reduction.

It must fit within legal and regulatory reality. A system that functions technically but cannot establish enforceable rights, compliant transfers, or clear accountability remains limited as institutional infrastructure.

It must be operationally usable. Institutions need custody, permissions, auditability, reporting, cybersecurity, governance, vendor reliability, and internal controls.

Finally, it must be resilient. Financial infrastructure cannot depend entirely on temporary incentives, opaque governance, fragile bridges, speculative liquidity, or the assumption that market conditions will remain favorable.

No single criterion is enough.

A technically elegant system without legal clarity is incomplete. A compliant system without liquidity is commercially weak. A fast settlement network without trusted custody or effective controls introduces risks that institutions may be unwilling to accept.

The product is the complete architecture.

Stablecoins offer one of the clearest examples of the shift from narrative to infrastructure.

Their first important role was relatively narrow: they provided crypto markets with a dollar-like asset that could move between exchanges and blockchain networks without depending entirely on bank transfers or conventional operating hours.

That function made stablecoins essential to digital asset trading.

But the more consequential development is what happens as the same capability moves beyond trading.

A dollar-denominated instrument that can settle quickly, move across borders, integrate with digital wallets, and be embedded into software has implications for payments, remittances, fintech applications, corporate treasury, on-chain capital markets, and access to dollar-based value.

The serious question is no longer whether stablecoins are “digital dollars.” It is whether particular stablecoin systems can serve as reliable settlement instruments.

That requires more than a token contract. It requires credible reserves, dependable redemption, issuer governance, distribution, liquidity, regulatory oversight, payment integration, sanctions controls, cybersecurity, and interoperability with banking and accounting systems.

Stablecoins do not automatically replace bank deposits, card networks, or conventional payment infrastructure. They introduce their own concentration, liquidity, consumer-protection, illicit-finance, and systemic risks.

But their development illustrates the core infrastructure pattern: a crypto-native workaround begins inside digital asset markets and gradually evolves into a broader financial rail.

The broader design is best understood through The Stablecoin Stack, where issuance, reserves, distribution, settlement, compliance, and integration operate as parts of the same system.

Stablecoins introduce a different payment architecture from traditional card networks, particularly where blockchain rails combine the transfer of payment instructions with the movement and settlement of value.

Tokenization has also suffered from narrative excess.

The declaration that “everything will be tokenized” is too broad to be useful. Many assets already move efficiently within existing systems. Others are constrained by securities laws, tax treatment, investor eligibility, custody requirements, transfer restrictions, or contractual terms that do not disappear when a digital record is created.

Tokenization matters when it improves the issuance, administration, transfer, financing, transparency, or use of a financial claim.

That is why tokenized Treasury products, money market funds, private-credit interests, collateral instruments, and fund shares have become more consequential than many early experiments in tokenized ownership. They connect blockchain-based administration to recognizable assets, established pools of capital, and identifiable financial needs.

But the blockchain record is only one part of the structure.

What asset backs the token? What rights does its holder possess? Who issues it? Who maintains the authoritative ownership record? Who can transfer it? How are investor restrictions enforced? How is income distributed? How does the token interact with custodians, broker-dealers, transfer agents, accounting systems, and insolvency law?

These are not implementation details surrounding the product.

They are the product.

In institutional tokenization, the legal architecture of tokenized assets is at least as important as the blockchain layer. A token cannot create rights that the surrounding legal structure does not recognize. Understanding what ownership of a tokenized asset actually means therefore requires examining the legal claim, issuer structure, records, custody arrangement, and enforceability behind the token.

This is why custody becomes a strategic boundary. Institutions must know not only where an asset is recorded, but who controls it, how that control is protected, what happens if an intermediary fails, and whether the holder’s claim can be enforced.

Early crypto culture often portrayed compliance as an external constraint—something imposed on an otherwise open and self-contained system.

That posture is incompatible with institutional scale.

When digital assets become part of payments, securities markets, treasury operations, fund administration, or cross-border financial activity, compliance becomes part of the infrastructure. It cannot remain an afterthought. It has to become part of the system’s design.

Identity verification, sanctions screening, transaction monitoring, transfer restrictions, audit trails, reporting, permissioned access, and jurisdiction-specific controls increasingly determine whether a system can move from experimentation to repeatable use.

In some institutional settings, the important innovation will not be maximum openness. It will be programmable compliance: the ability to apply rules directly to issuance, custody, transfer, and settlement workflows.

This does not mean that every digital asset network must become centralized or permissioned.

The mature market will be plural. Public networks, permissioned systems, regulated intermediaries, and hybrid architectures will coexist. Retail trading, decentralized protocols, tokenized securities, enterprise settlement networks, and regulated payment systems will use different combinations of trust, control, and openness.

The serious question is not which model is ideologically pure.

It is which architecture is appropriate for the use case.

Narrative markets tend to place the token at the center of the economic story.

Infrastructure analysis takes a wider view.

Value may accrue to settlement networks, stablecoin issuers, custodians, compliance providers, wallet infrastructure, tokenization platforms, data services, oracle networks, market makers, trading venues, asset managers, banks, or software providers that connect blockchain rails to existing financial operations. This wider distribution of economic benefit is examined in Where Value Accrues in the Crypto Stack.

In some cases, value will accrue to token holders. In others, it will be captured by companies, intermediaries, platforms, or incumbent financial institutions that use blockchain infrastructure without exposing customers directly to a token.

That distinction is essential.

The success of digital asset infrastructure does not guarantee the success of every investable crypto asset associated with it.

The internet transformed commerce, media, and communication, but countless internet companies failed. Cloud computing became foundational to enterprise technology, but economic value consolidated around a relatively small number of platforms, software ecosystems, and infrastructure providers.

Digital assets are likely to follow a similar pattern.

The infrastructure may be real even when many of the tokens are poor investments. A protocol may process meaningful activity while its token captures little of the resulting economic value. An enterprise may benefit from blockchain-based settlement while its customers remain unaware that the technology is being used.

Markets often price the story first.

Economies reward the infrastructure later.

Institutional adoption is often imagined as a single transformation: traditional finance suddenly “moves on-chain.”

That is unlikely to be how the transition occurs.

Financial institutions adopt new infrastructure selectively. The benefit must be sufficient to outweigh switching costs, integration work, legal uncertainty, operational risk, reputational exposure, and the difficulty of changing established systems.

Adoption will therefore emerge first where current infrastructure is especially inefficient or where blockchain-based systems create a clear advantage.

That may include stablecoin settlement in particular payment corridors, tokenized cash and collateral, Treasury and money market products, fund administration, private-market distribution, digital asset custody, cross-border business payments, or controlled forms of institutional DeFi. These early enterprise stablecoin use cases show how adoption can begin through targeted treasury, settlement, payment, and accounting workflows.

The movement will be incremental.

A bank may partner with an infrastructure provider before building its own platform. An asset manager may first use tokenization as a new distribution channel rather than replacing its entire fund structure. A treasury department may adopt stablecoins for a limited set of cross-border transfers while retaining conventional systems for most activity.

The important signal is not the announcement of another pilot.

It is the appearance of repeatable workflows.

Real adoption begins when an institution uses a system more than once, integrates it into ordinary operations, allocates continuing resources to it, and expands its use because it produces a measurable advantage.

That kind of adoption is less visible than a token launch. It is also more durable.

An infrastructure market produces different signals from a narrative market.

Token prices and market sentiment still matter, but they do not tell the whole story. A more useful analysis watches whether stablecoin regulation creates workable pathways for payment and treasury use; whether tokenized funds attract continuing capital; whether banks build, buy, or partner for digital asset capabilities; and whether custody, compliance, accounting, and reporting systems become easier to integrate.

It watches whether liquidity for tokenized assets develops beyond isolated venues. It asks whether on-chain records connect clearly to off-chain legal rights. It distinguishes pilots from recurring activity and technical demonstrations from economically meaningful workflows.

Above all, it asks whether a blockchain-based system reduces a real cost, removes a genuine source of friction, or creates a capability that could not be delivered as effectively through existing infrastructure.

Those are the signals that matter when a market begins to mature.

Crypto will always produce narratives.

Markets need stories. Builders need visions. Investors need frameworks. Media organizations need headlines. Narratives will continue to influence prices, attract talent, and direct capital toward new areas of experimentation.

But the next phase of digital assets requires a different standard.

The most important developments may not be the loudest. They may look like a stablecoin embedded inside a fintech payment workflow, a tokenized Treasury product used as collateral, a custody platform earning institutional trust, a compliance system making transfers safer, or a settlement network quietly reducing the need for reconciliation.

That is not as dramatic as a bull-market slogan.

It is how infrastructure changes.

The future of digital assets will not be determined only by ideology, speculation, or branding. It will be determined by whether these systems can become useful, trusted, compliant, liquid, resilient, and economically superior in specific contexts.

That is the thesis behind Blocks & Bonds.

The market is moving from crypto as narrative to digital assets as infrastructure.

And that is where the real story begins.

Understanding the shift from narratives to infrastructure is only the first step. The next question is where economic value is actually captured as digital asset systems mature.

Read Where Value Accrues in the Crypto Stack to see how value moves across settlement networks, stablecoin issuers, applications, custodians, liquidity providers, and token holders.